log in

log in“Since 2007, the share of all banking assets controlled by the largest six banks grew from 90% to 93%.”—John Jason, C.D. Howe

*******

Fine time to land a crushing regulatory uppercut on bank challengers.

That’s what the good intentioned folks in Ottawa did this week when they turned the tables on borrowers and mortgage competition. (Those details) In doing so, the Finance Department left borrowers as confused as a hungry baby on a topless beach.

People are now racing to grasp what happens next, and make no mistake, this has become a fight. It’s the regulators versus Canadian borrowers. We turned to the legendary Clubber Lang for a prediction on how consumers will fare:

The DoF has been training hard for this bout. It’s got three key pieces of data in its corner.

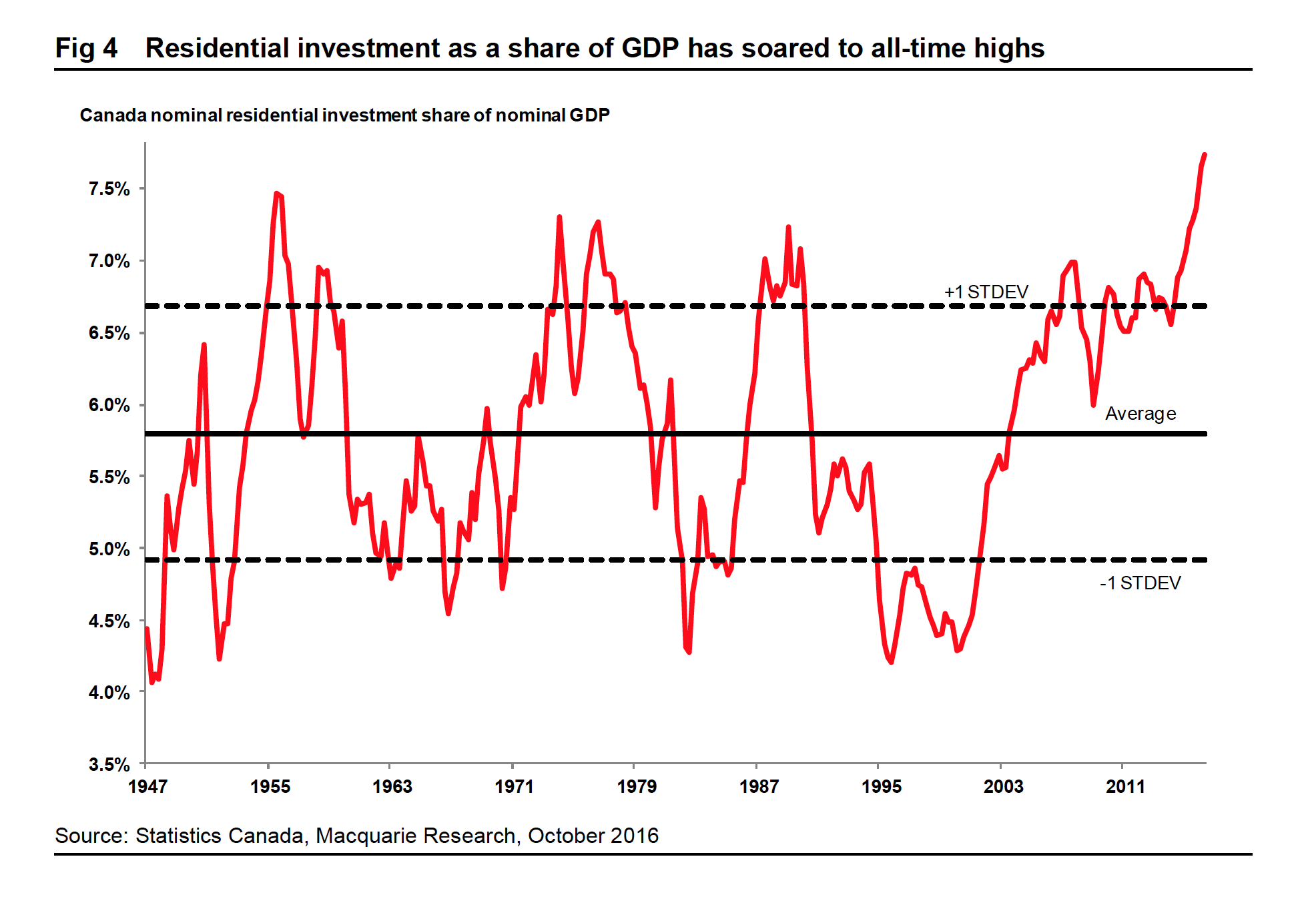

1) The Canadian economy’s concerning over-reliance on housing…

Source: Macquarie Research Canada

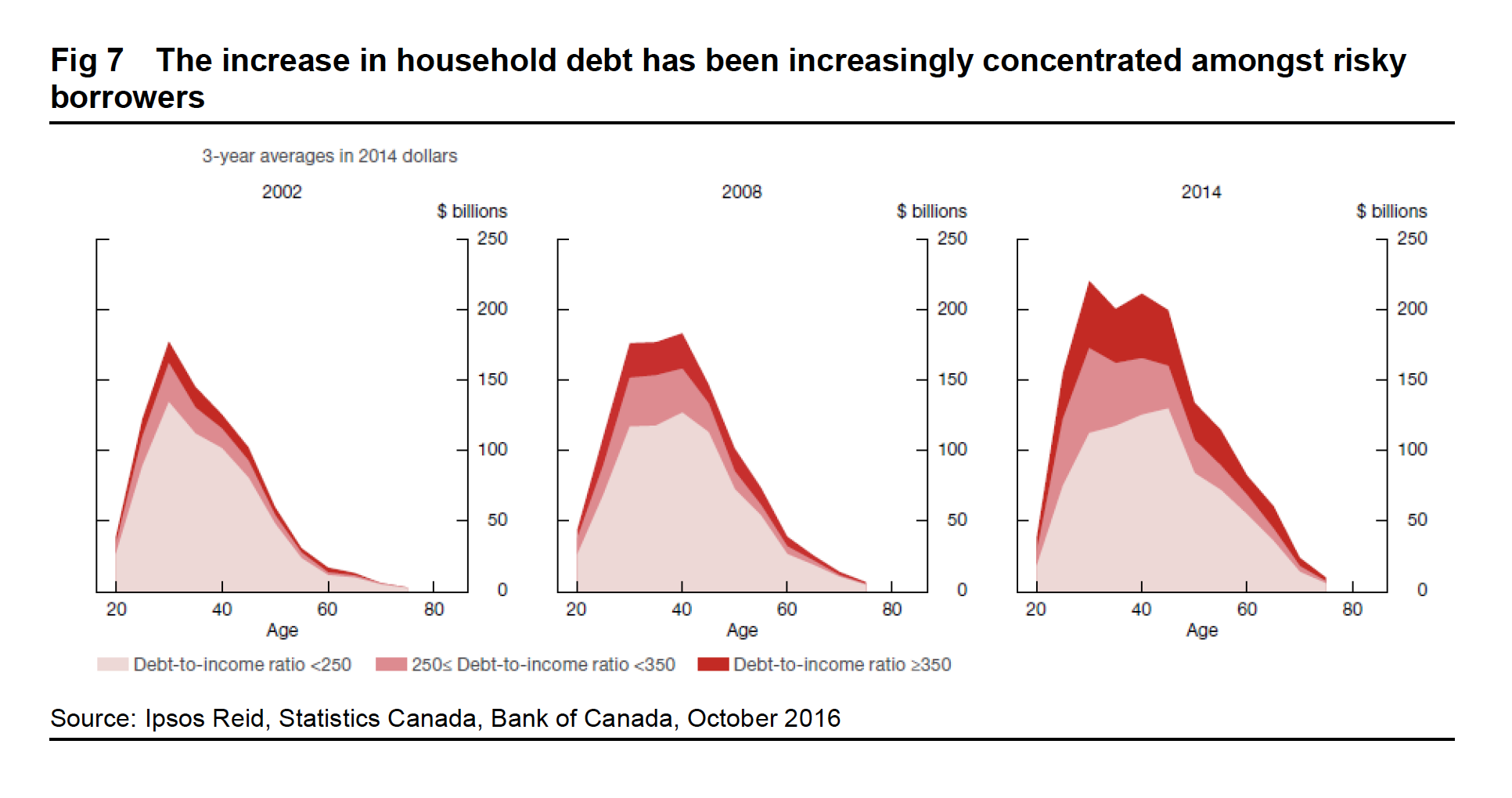

2) Borrowers’ growing debt addiction…

Source: Macquarie Research Canada

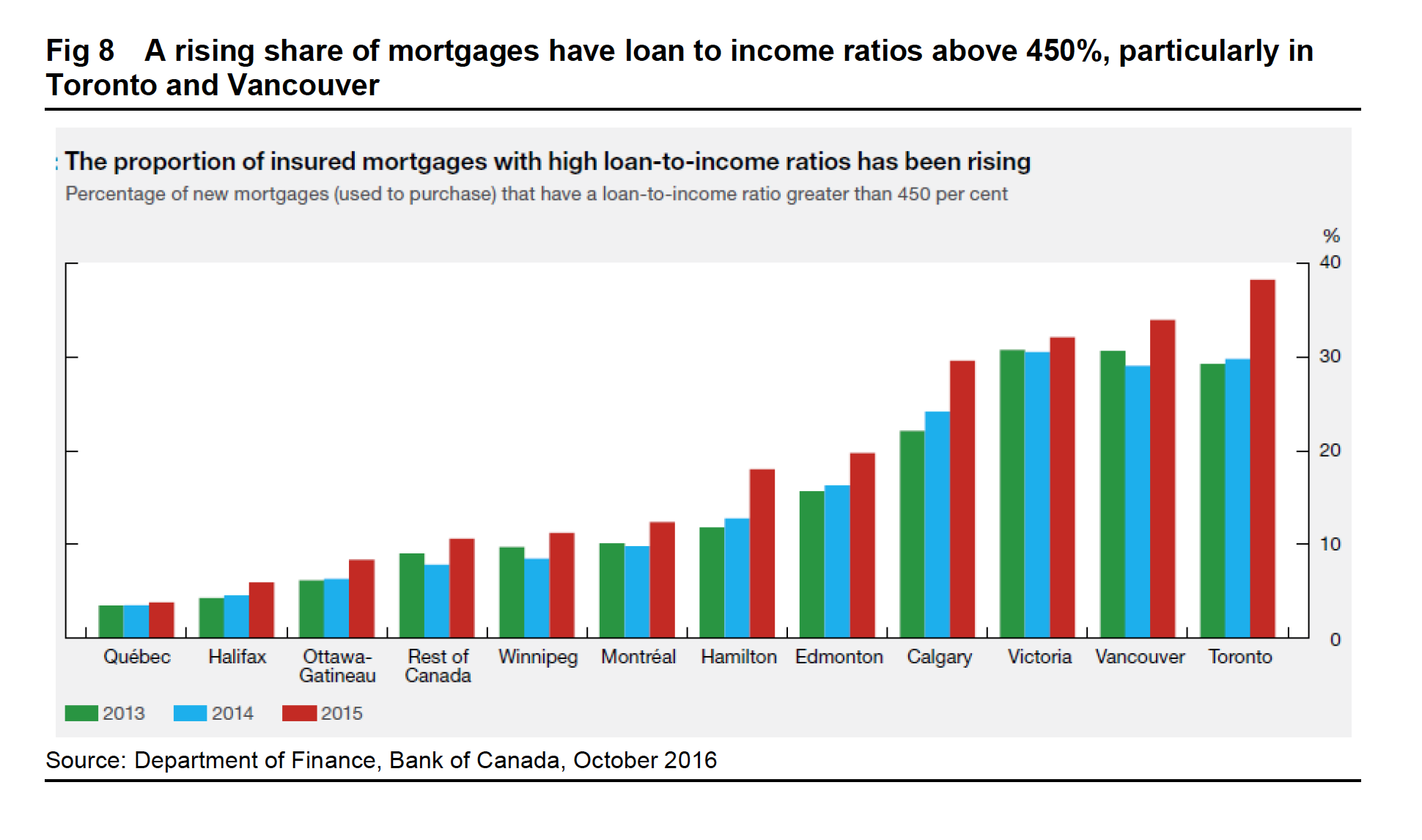

3) Deteriorating fundamentals on insured mortgages.

Source: Macquarie Research Canada

So it’s hard to argue that big brother shouldn’t have acted. It’s how our puppet-masters pulled the strings that may cost them public trust. There are lots of strings they could have pulled besides these ones, not the least of which is boosting credit requirements on low-equity and below-average credit borrowers.

Now on to the victors in this bout…

The winners, by TKO, are hereby…

The winners, by TKO, are hereby…

- RBC, TD, Scotiabank, BMO, CIBC and National Bank

- And anyone else who doesn’t need to insure mortgages in order to sell them to investors (e.g., some credit unions).

- The biggest mortgage finance companies (MFCs) might also do okay. We’re talking the likes of First National, MCAP, etc. They have the strongest bank funding relationships and will mop up business lost by smaller insured-only lenders.

- By the way, don’t blame the banks for this. It’s not like they emailed the banking regulator and said “Can you please make it harder on my competitors to do business?” That’s ridiculous. They never would have used email.

- Anyone buying with less than 20% down (a.k.a., a “high-ratio” buyer)

- Lenders about to lose first-time buyer business, refinances, rentals, $1 million+ mortgages and extended amortizations will have to feed more on purchases with sub-20% down payments.

- This will fuel rate competition to new extremes on “high ratio” mortgages.

- It’s been like this for a while (check the best 5-year fixed rates on the Spy; they’re almost 10 bps below conventional rates). You better believe, if high-ratio competition was trench warfare before, now it’s gonna get downright medieval.)

- Skill-testing question: How do you put more skin in the game and get a worse interest rate? The answer.

- Non-prime & CU lenders

- Assuming banks are forced to adopt the posted qualifying rate on low-ratio mortgages (I think they will) and are forced to cap all amortizations at 25 years (I think they might be), then only non-prime lending sources and credit unions will offer these flexibilities, and they’ll charge a premium for them.

- Anyone scared about a housing crash

- You’re getting an incrementally less risky housing market long term, in exchange for a riskier housing market short term, higher interest costs and fewer lender and product options.

- Is that a fair trade? Our trusty regulators think so, but allow me to pose an apparently outlandish concept. (Wait a minute while I climb up on the soapbox.) What if we had both a lower-risk housing market and the lowest possible borrowing costs—supported by our sovereign’s guarantee—for deserving prudent Canadians? Regulation doesn’t have to be an “or” proposition. The alternative: Charge over-indebted, low-equity, below-average-credit-score borrowers higher rates and insurance premiums to weed them out. Then cut a break to hard-working families with pristine credit, strong employment, manageable debt loads, but higher housing costs. Regulators save face, decelerate housing and de-leverage riskier borrowers, and the rest of us get to retire quicker instead of adding another layer of gold plating to Bay Street’s toilet handles.

The big losers:

- Most other lenders

- Refinancers and first-time buyers account for over half of some MFCs’ business. Those poor saps are now stripped of their ability to compete in many cases.

- Meanwhile, compared to banks, the mortgages that MFCs originate have half the risk. Which borrowers does it benefit to take them out of the game? (The first person to answer this question intelligently gets a free dinner on the Spy. Hint: It’s a rhetorical question.)

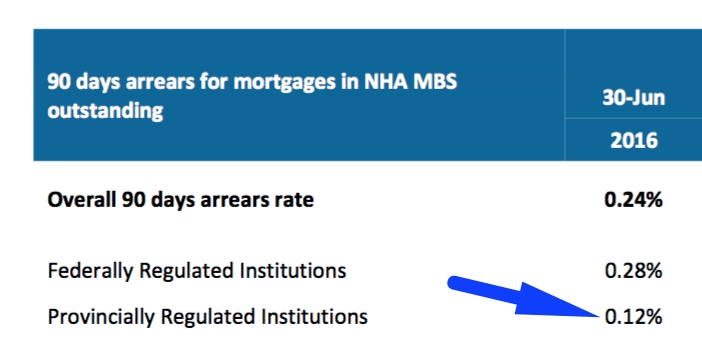

Source: CMHC

- Anyone renewing who has a modestly tight or tight budget

- The Department of Finance tells me that folks with active default insurance on their mortgage will not be required (by the rules) to prove they can afford a payment at the Bank of Canada’s 5-year posted rate when they switch lenders. The condition is, their mortgage risk cannot increase at renewal (e.g., their loan amount and amortization must stay the same).

- But, and this is a mega but, many lenders’ internal policies will still require borrowers to prove they can afford that posted-rate (4.64%) payment, even though:

- the person’s actual mortgage rate is over 2%-points lower, and

- the borrower has the safety net of refinancing into a lower payment if rates do surge.

- If you can’t qualify elsewhere at renewal, guess what? You get the rate your lender spoon feeds you. And even better, your lender ain’t no country bumpkin. It’s got big data on you, baby. It knows your credit habits, employment situ, bank balances, you name it. If it senses you won’t qualify elsewhere thanks to Ottawa’s new rule, it’ll use that information against you like a life insurance company charges higher premiums to smokers. Believe me. Lender retention departments are cracking the champagne and doing a party dance as we speak.

via GIPHY

- Anyone buying who has a somewhat tight budget

- The posted-rate qualification rule has already been widely reported so we won’t beat it to death. But National Bank Financial said today, “a homebuyer with a gross debt-service ratio (home carrying costs divided by income) of 32% or higher today would not qualify for mortgage insurance tomorrow.” That’s because the current GDS limit is 39% and the new rule (it thinks) could boost typical debt ratios by 7 percentage points.

- I’ve seen other bank analysts estimate closer to a 4- and 5-point impact on GDS, but it depends on the borrower assumptions. Whatever the number, value-shopping home buyers better get used to longer commutes. Urban sprawl, here we come.

- By the way, if I had to compile all the estimates I’ve heard from lenders, economists, the government and so on, somewhere around 10-15% of buyers may have to indefinitely defer purchases until they save bigger down payments, earn more income, get a co-signor or buy a cheaper property.

- Anyone who wants a refinance

- Fewer lenders will offer them and at higher interest rates.

- Refis are a $44 billion market. Those borrowers who can’t qualify for a refinance (because of the posted-rate qualification rule or maximum amortization reduction) may be stuck with an “alternative lender” who doesn’t insure its mortgages but charges another pound of flesh in rate.

- Or better yet! There’s always riskier high-interest unsecured credit, interest-only HELOCs and 20%-interest credit cards for shut-out mortgagors to fall back on. “Freedom 75” is starting to sound good.

- Even refinancers who qualify with flying colours are about to part with more money. Non-bank lenders—who brokers use to “buy down” interest rates—are starting to jack up their refinance pricing by 15 basis points or more, or suspend refis indefinitely.

- Anyone who wants a $1 million+ mortgage

- Big banks and maybe a handful of large credit unions will become even more dominant in super-jumbo loans. With less competition, mortgage rates (once again) have only one way to go.

- Anyone who wants a rental-property mortgage

- Some lenders have already stopped all rental financing that closes after November 15 or 30. Others have imposed 15-25 basis point rate premiums.

- Side note: This doesn’t apply if you live in the property being rented (e.g., if you have a legal basement rental suite).

- Anyone who wants an amortization over 25 years

- Come December, fewer lenders will let you am’ out your mortgage over 30 years (mostly banks and credit unions). We’re already seeing MFCs starting to quote 10-basis-point rate premiums for them, and limit long-amz to purchases only (no refis or switches). And if you want to refinance a rental property to 80% loan-to-value with a long amortization at best rates, good luck with that.

- 35-year amortizations may also go the way of the dodo. At the very least, post-November 30, there will be far fewer providers. The ones that remain (if any) will charge a much higher toll for these exclusive products. Betchya a buck that the DoF’s assault on amortizations pushes tens of thousands into interest-only HELOCs (a long-amortization substitute if you want the lowest possible payments).

- Anyone who’s self-employed and can’t prove income traditionally

- Folks who pay themselves but don’t have traditional pay statements and job letters rely on BFS (Business for Self) mortgages. Insured BFS mortgages are now dead like dirt. Once again, insured-only lenders will have to sell these loans to Mr. Banker and pass along his juicy rate premium to borrowers.

- We’re already starting to see up to 40-basis-point rate surcharges on these products. That’s $5,600 extra interest on a 5-year $300,000 mortgage.

Essentially, the DoF has turned the mortgage expressway into a two-lane highway with a roadblock. It could have just ticketed the speeders and let the prudent drivers pass.

Essentially, the DoF has turned the mortgage expressway into a two-lane highway with a roadblock. It could have just ticketed the speeders and let the prudent drivers pass.

Of course, banks can still offer most of the options that MFCs are losing. The billion-dollar question is, will banks now:

a) undercut their more vulnerable competitors to swipe share; or,

b) seize this opportunity to jack up rates and improve profits, as they so deeply desire?

Once I dust off my game theory textbook I’ll let you know. As of October 7th, the guess is that they’ll do a little of both, but more of the latter.

Here’s one thing we do know: The bank regulator is considering imposing the posted qualifying rate on conventional mortgages and limiting all bank mortgages to 25-year amortizations. If that came to pass, it could happen as soon as Ottawa’s finished revising “Guideline B-20” (the banks’ mortgage underwriting bible). But this could potentially take at least 2-3 quarters, lenders tell me. For my money, with all the critics out there accusing regulators of bank favouritism, I’ll take the under on that timeframe.

In the meantime, Clubber ain’t foolin. Homeowners are about to feel the pain.

12 Comments

Great stuff. Crash prices. Is anyone in Vancouver doing any work or is it all just credit creation through land? Pity Quebec will have to foot the bill for the wreckless credit creation elsewhere.

Housing prices shot up mostly because of cheap borrowing costs. Higher borrowing costs will lead to lower demand for McMansions and therefore lower housing prices.

For rental properties, even if 5yr fixed rates go to 3%, they are still a great investment. The 4% CCA rate gives you a great way to turn high-taxed income into low taxed capital gains in the future.

Frankly I don’t care why home prices went up. I’d take 0% rates if it would add another $100,000 to my home equity. We’re getting ready to sell and will pocket a nice tax-free capital gain. I just hope these absurd rules don’t take prices down 5% to 10% before we can get out.

i would love a flow chart on this… and even some diagrams… thick read.

So the blockheads in power tax us to death and now make us pay more for a mortgage. I’m so glad they don’t have to worry about any of this on their fat government salaries. When will these unaccountable bureaucrats be satisfied? When families are left with 20 cents disposable income for every dollar earned?

Seems some think high prices are free money. The next generation has to take on more debt for your u earned profit.

Unless the general level of interest rates is rising, the government has no business raising mortgage costs. Its job is to protect us from risky borrowing, not pick winners and losers in the mortgage market.

I’m just going to play devil’s advocate for a moment, but what do you guys think would have happened if the government didn’t step in and do something to gradually cool the market? We were (maybe still are) on track for an unavoidable housing crash.. double-digit price growth can’t go on forever. I get that the changes may not be perfect, but would it have been better to do nothing at all?

Regulators deserve credit for much of what they’ve done in prior years. If the feds hadn’t tightened in the past we’d potentially be facing unmitigated disaster. The question is only one of fairness of impact. Each rule change must be carefully evaluated on its own merits, and it looks like regulators spent about a half-hour evaluating the repercussions of this latest round of changes.

@Cool head

I don’t think anyone is disagreeing that there was room for more regulatory changes to assist in cooling the two most overheated markets: Toronto and Vancouver. You mention double-digit growth, but outside of those two metro areas, name me a place that is seeing that type of increase? Certainly not Calgary, Montreal, Windsor, Halifax, St. John’s, etc. etc.

I’d even go so far as to say the move to alter the qualifying rate makes sense. But definitely not at a rate that is more than twice the current 5 year fixed rates.

There is so much more that is wrong with these changes (new rules for monoline lenders) but I’ll leave it there for now. Time will ultimately tell how much damage this will do to the Canadian housing market and competition in the mortgage market.

But I do feel for all those otherwise well-qualified first-time buyers who pose minimal risk who are now facing one more huge and in many cases insurmountable obstacle to their dream of homeownership.

A few years ago, a 5-year fixed with 2.99% was causing headlines. People back then were already using the “low rates” to drive housing prices far beyond inflation. Even with a 50-basis-point increase, mortgages would still be cheaper than back then.

The competitive handicap for small lenders is regrettable. However, time and again there have been analyses coming to the conclusion that the only thing that will effectively slow the craze is higher rates. From that angle, the government is getting what it wants (and the risk reduction for public money is just a bonus on top of that).

One thing that I wonder about is, if default rates are already so low and the risk is this marginal, why do we still need the government to insure the investment? Couldn’t lenders do the same thing by charging an amount similar to what CMHC charges, and cover the risk cheaply without government involvement? I feel there is a disconnect somewhere – if the government raises its prices for insurance higher than what a fair market would bear, a private insurer should have the opportunity to make inroads instead. If no private insurer steps up for the same deal that we had, does this mean the government wasn’t pricing their insurance at fair market value? Why would we expect them to undercut the market when at the same time the current rate of housing price growth poses a risk to the health of our economy in the long run?

What I’m most interested in, though, is this:

What steps would *you*, dear Spy and long-term consumer-friendly mortgage expert, have taken to get the housing market (maybe only of Vancouver and Toronto) back into healthy non-bubble territory?

Hey Jacob,

Fundamental question #1 is, do we want to safely encourage mortgage competition? If we don’t, the bank-opoly will have a monstrous advantage (because they don’t need to insure conventional loans, because they have more securitization options, because they can fund with deposits, etc. etc.). Anyone who got a mortgage pre-1990s will recall how skimpy bank mortgage discounts were prior to the advent of mortgage finance companies and brokers. Most Canadians would argue that money is better left in their pockets than bank coffers. That’s exactly why the government backs the mortgage market, or at least, why it used to.

Fundamental question #2 is, is the small risk of cataclysmic defaults worth the rewards of government mortgage sponsorship. No one can answer this question without doing some math (but oh so many people opine nonetheless). The reality is, if you hypothesize a worse housing crash than the U.S. experienced, apply a reasonable probability to it, calculate the insurer’s losses, and then calculate the government’s (taxpayer’s) exposure, you’d find that the losses are significantly less than the savings Canadians enjoy through government mortgage sponsorship.

Canada is blessed with a triple-A credit rating. Ottawa can and should use it to save Canadian families as much interest expense as is reasonably possible. That said, no one wants a Toronto/Vancouver disaster. So yes, let’s find ways to temper demand from less qualified buyers and high-risk refinancers. There’s no shortage of solutions, including but not limited to applying stricter qualifying rules to those with small down payments and/or weaker credit and/or properties in overvalued markets. Doing so would reward prudent Canadians with savings and more financing choices, and simultaneously achieve the Feds’ aim of “de-risking” the mortgage market. Cheers…