log in

log inEffective this week, it gets a little easier to buy a house or refinance.

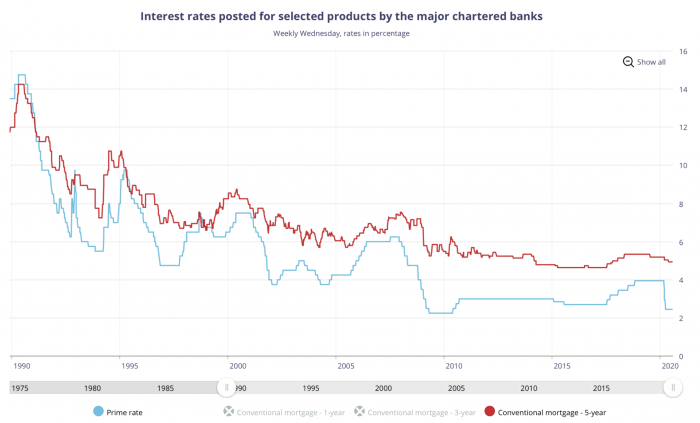

On Saturday, BMO and CIBC shaved 15 basis points off their posted 5-year fixed rates. That’s enough to drop the benchmark 5-year posted rate to 4.79%.

Given regulators use this benchmark rate to calculate Canada’s minimum mortgage stress test, today’s cuts mean you’ll now need less income to qualify for a given mortgage amount.

Put another way, it means someone making $70,000 a year can now afford a 1.2% ($4,000) more expensive home with 5% down. That’s not much to get excited about but on a market-wide basis, small buying power improvements are inflationary for home prices, other things equal.

These moves put the benchmark 5-year posted rate just 15 bps above its all-time low of 4.64%. That rate was last seen three years ago in July 2017.

Here’s a summary of each bank’s changes:

- BMO has lowered the following posted fixed rates:

- 2yr: 3.39% to 3.29%

- 3yr: 3.89% to 3.75%

- 4yr: 4.34% to 4.24%

- 5yr: 4.94% to 4.79%

- 6yr: 5.44% to 5.24%

- 7yr: 5.55% to 5.40%

- 10yr: 5.95% to 5.80%

- CIBC lowered the following posted fixed rates:

- 3yr: 3.69% to 3.59%

- 4yr: 4.34% to 4.24%

- 5yr: 4.94% to 4.79%

- 7yr: 6.00% to 5.90%

- 10yr: 6.19% to 6.09%

- CIBC also trimmed the following “special” rates:

- 5yr fixed (high ratio): 2.22% to 2.07%

- That’s the lowest widely advertised 5-year fixed rate ever from a Big 6 bank.

- It’s now a race to see which of Canada’s mega-banks will be first to 1.99%. In reality, for well-qualified borrowers, most banks have been sub-2% on insured mortgages for weeks. They’ve just refused to advertise it.

- 5yr fixed: 2.39% to 2.24%

- The lowest widely advertised refinance rate from a Big 6 bank.

- The leader is still Tangerine at 1.99%.

- 7yr fixed: 2.81% to 2.71%

- 5yr variable (high ratio): 2.13% to 2.03%

- 5yr fixed (high ratio): 2.22% to 2.07%

10 Comments

Don’t banks realize they are losing customers by not advertising competitive rates?

The penalty goes higher now, but the interest is also lower. Hope they can be balanced.

Hi Spy,

Where should the stress test rate be if we were in more normal times?

Hey Tom, Yes, they do. But banks feel that not showing their hands is the best way to maximize profit margins.

This mindset is slowly changing however. Witness Scotia’s eHOME for example. Once big banks lose enough market share to the likes of HSBC and others, they will have to change their approach.

That’s right Shawn. Falling short-term fixed rates widen interest rate differentials. That costs a lot of people a lot of money when they go to break their mortgages early.

Hi ZhangE,

When OSFI dreamt up the stress test, it expected banks to keep their 5-year posted rates roughly 200 basis points above typical uninsured 5-year fixed rates. Prior to this week’s change, Canada’s benchmark rate was approximately 250+ bps higher than typical 5-year contract rates.

Based solely on historical norms and today’s rates, the benchmark rate (minimum stress test rate) should be closer to 4.29%, as opposed to 4.79%.

The [unofficial] interest rate for insured mortgage with cibc is 1.82% now

Thanks Paul

Is this fixed / variable and on which term

My wife and I just renewed with TD in Edmonton. We agreed to a three year fixed portable at 1.92.

I used the insight extracted from Rate Spy updates to negotiate with our bank.

The last offer before this fixed rate was a 1.92 variable open so we took the sure thing.

The hassel of reapplying and requalifing with another lender keeps this customer with TD.

There would have also been fees charged by a new lender for a new mortgages that were also in the back of our minds?

Ratespy – Would this be the reality?

Thank you Rate Spy

Hi Alan, Those fees and hassle usually work in the incumbent lender’s favour at renewal. They’re well aware that most renewing borrowers feel the same way and it impacts the renewal rates they offer.

In practice, switching needs to make economic sense. Most lenders pay some or all of the switch costs, depending on the mortgage type and borrower. But even so, if you have a small balance and/or short remaining amortization, or you simply like your existing mortgage terms/features, even a free switch often isn’t worth the effort.