log in

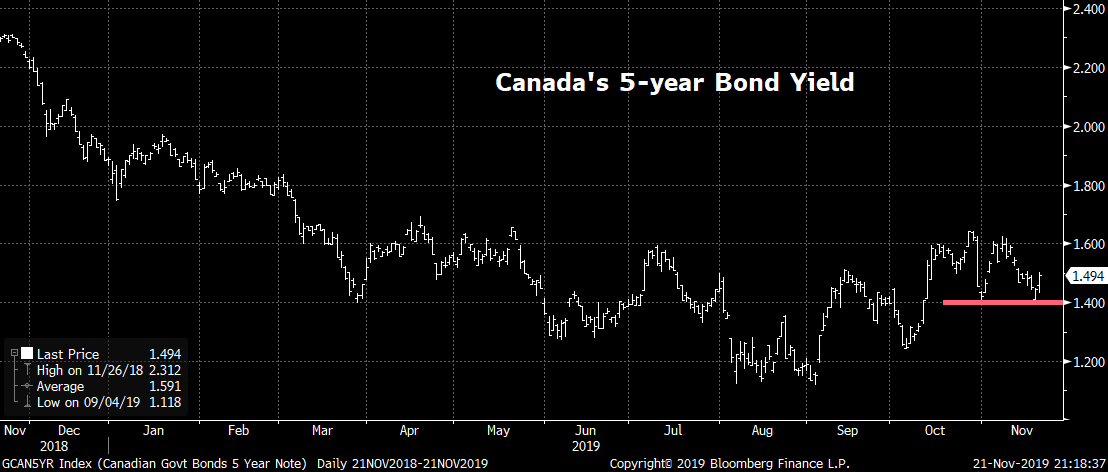

log inCanadian government bond yields, which lead fixed mortgage rates, are essentially adrift at sea.

They, like so many other global yields, seem to just be biding time until positive (or negative) trade news breaks out of Washington.

There’s so much uncertainty out there that it makes even less sense than usual to try and time the market. When President Trump is finally ready to sign a U.S.-China trade pact, rates may shoot up 20-30 bps on the positive economic implications, but they won’t stay elevated forever.

In the Short Term

The levels of the 5-year bond to keep an eye on are:

- 1.40%: A few days in the 1.30s or below that should take the lowest 5-year fixed rates down again

- 1.70%: Multiple days above that number should lift the lowest 5-year fixed rates at least 5-10 basis points

Medium Term

The next few years are the hardest to predict. We’ll leave that to the prestigious yet fallible investment banks like Goldman Sachs—who, by the way, is calling for a mini-bear market in bonds next year. Given bond prices and rates move oppositely, that implies higher interest rates.

If that does transpire, few expect a steep, relentless climb in rates. Just last week, BoC Governor Stephen Poloz called Canadian rates “about right.” Investors responded by trimming their rate cut expectations in 2020 to just one.

If you filter all the bullish and bearish noise, however, the safest assumption is a modest change in rates in either direction. Certainly not enough to dramatically alter your mortgage term selection.

Longer-Term

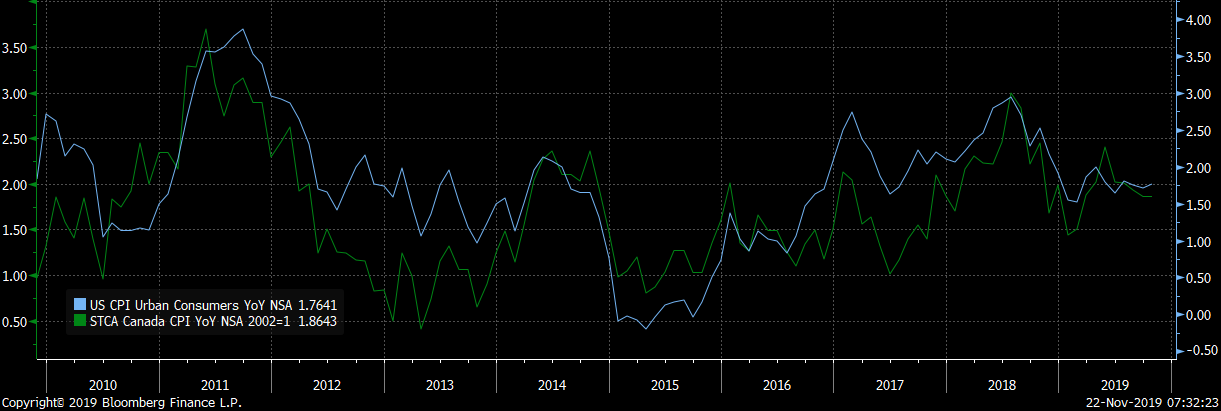

Canada’s 5-year bond tracks U.S. bonds about 70% of the time over the long run. So if you want to know what’ll happen to our rates, read U.S. economic headlines. That’ll hold true until there’s a market decoupling of the two countries (perhaps due to a market shock, like plunging oil prices).

Inflation expectations will continue setting the tone. And as the chart below shows, Canadian inflation tends to move with price increases south of the border.

Looking out 10 years, investors expect inflation at or below 2%. Indeed, the market has “completely discounted inflation as a risk and therefore it’s become a risk,” said JP Morgan’s Oksana Aronov on Bloomberg’s Real Yield this week.

The problem with that? “…You need very marginal changes….to change the sentiment” and significantly move rates, she said.

Rate Nuggets

- Inflation may be further away from the Bank of Canada’s target than some think.

- Poloz: New tech is keeping a lid on inflation, and rates

- Penalties can throw a wrench in plans to refinance to a lower rate

- CMHC’s Siddall again suggests he’d be willing to re-evaluate the $1 million property value cap for default insurance

- TD: “…Financial stability concerns mean that the bar to rate cuts is higher than it would otherwise be”

1 Comment

I can’t see anything getting us back to the sunny days of +4% annual GDP. Those years are long gone. Just keep taking the lowest rate you can find and you can’t go wrong.