log in

log inAnother Bank of Canada rate meeting has come and gone with no shift in prime rate.

Another

Another Here’s pretty much the only line in the Bank’s 421-word statement worth repeating: “On balance, risks to the profile for inflation have tilted somewhat to the downside…”

Deciphered, this means: The Bank is closer to dropping rates than raising them. And it could take multiple rate meetings before that bias changes.

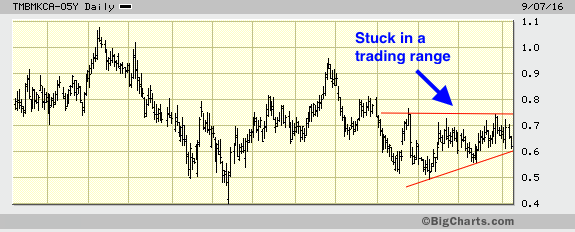

In the meantime, keep an eyeball on 5-year bond yields. Yields drive fixed mortgage rates and they’re presently coiling up in what Bay Street types call a “trading range.”

Daily chart of Canada’s 5-year bond yield, via BigCharts.com

In fact, the 12-month range for Canada’s 5-year yield (based on monthly closing prices) is just one basis point from the lowest it’s been in decades. It’s almost like the quiet before a storm. We just don’t know if the storm (next big rate move) will blow up or down.

Either way, it would probably stun the market if rates moved much more than 15-20 basis points near-term. Hence, don’t bother waiting in anticipation before pulling the trigger on your mortgage application. If rates fall materially, most lenders will adjust your rate lower by default. If yields break to the upside, a rate hold is your best protection.