log in

log inDon’t worry about the nagging side effects from the federal mortgage stress test.

You might have heard about them in the media, but based on recent stats shared by the banking regulator, they’re overblown. Nothing to see here…

Well, actually, there is more to see. OSFI’s latest assertions raise just as many questions as answers. Here were six points from its January 24 speech that warrant deeper analysis.

#1) The Long Arm of the Stress Test

Federally regulated lenders “hold nearly 80% of all residential mortgages issued in Canada,” OSFI said. In turn, the federal mortgage stress tests apply to roughly four out of five mortgage borrowers.

The impacts on real estate and the economy are, therefore, far-reaching. For that reason, parliament cannot be complacent in assuming that the rule-makers who designed the stress test created optimal policy.

#2) Trying to Justify Stress-testing Switches

OSFI has felt it necessary to publicly defend its application of the stress test on lender switches once again. That’s at least four times now. (A switch is when you change lenders at maturity with essentially no increase in mortgage risk.)

The regulator explained that it “does not require the re-underwriting of existing mortgages when they come up for renewal.” It “sees this as a reasonable practice.” And it is.

But, should a borrower want to change lenders to get a better deal, OSFI demands that the new (competing) lender apply the stress test.

Critics say this is unfair because it blocks borrowers with higher debt ratios from switching lenders to lower their debt burden. For this reason, countless consumer advocates have pressed OSFI for an exemption to the stress test for renewing borrowers. (More on this)

Critics say this is unfair because it blocks borrowers with higher debt ratios from switching lenders to lower their debt burden. For this reason, countless consumer advocates have pressed OSFI for an exemption to the stress test for renewing borrowers. (More on this)

OSFI justifies its position by saying lenders should not “rely on the past underwriting standards of another lender.”

But that’s a red herring, some charge, given that all prime lenders fully underwrite every single new borrower. When borrowers switch lenders, the underwriting is far more thorough than what the incumbent lender does when it simply renews an existing borrower.

The proposed exemption would simply reduce the stress-test rate on switches from the current rule (which is the greater of the contract rate + 200 bps or the benchmark rate) to simply the 5-year fixed contract rate.

That’s okay, because borrowers availing themselves of this exemption would have already proven they pay on time (which is highly correlated with continued timely payments) and would already meet all other underwriting standards.

Concerned observers believe that the Finance Minister owes it to Canadians to rethink this part of the stress test, but we may have to wait for a new government for any progress in this area.

#3) Reported Rates at Renewal are Misleading

OSFI says, “Concerns have been raised that the stress test could limit a borrower’s ability to obtain competitive rates at renewal.”

That would be a valid concern.

But the regulator counters, “…Data from OSFI regulated lenders shows that following the introduction of the revised [B-20] guideline, the difference between renewal and new mortgage rates for uninsured five-year fixed and variable-rate mortgages has remained largely unchanged.”

But the regulator counters, “…Data from OSFI regulated lenders shows that following the introduction of the revised [B-20] guideline, the difference between renewal and new mortgage rates for uninsured five-year fixed and variable-rate mortgages has remained largely unchanged.”

But, interestingly, the regulator has admitted in the past to not specifically measuring the renewal rates paid by borrowers who had high total debt-service ratios (e.g., > 40%). Those are the individuals who would be most prone to paying higher rates at renewal. They are the borrowers lenders would be less willing to negotiate with.

What’s more, if such borrowers (a minority) did in fact pay higher rates, those higher rates could conceivably be offset by falling rates paid by the majority of other well-qualified borrowers. That is indeed plausible given how competition has intensified over the past two years.

Either way, OSFI’s own data show an increase in interest rates at renewal relative to rates on new mortgages. The extra that renewers paid in 2019 averaged 0.12% versus just 0.05% in 2017, the year before the revised guideline. Given that high-TDS borrowers are a small percentage of the market, that 0.07% renewal rate increase is meaningful and should not be downplayed.

#4) HELOC Concerns

OSFI says it’s interested in “how lenders’ HELOC account-management programs track the portions of” readvanceable mortgages that are “re-advanceable.” It’s especially concerned when those credit lines are greater than 65% of the loan-to-value.

In English, this means OSFI is worried that credit limits might become inappropriate on HELOCs linked to a mortgage.

Their fear is that banks aren’t adequately monitoring property value and adjusting the borrower’s revolving HELOC credit limit (to ensure it stays under OSFI’s 65% LTV limit).

Their fear is that banks aren’t adequately monitoring property value and adjusting the borrower’s revolving HELOC credit limit (to ensure it stays under OSFI’s 65% LTV limit).

This is a legitimate concern if property values dive because people could end up borrowing high amounts relative to their home value.

This could lead to a “greater persistence of outstanding balances,” an OSFI spokesperson told RateSpy. “Compared to traditional mortgages, these [readvanceable mortgages] would be more vulnerable to a changing economic environment (unemployment, interest rates, house price shocks).”

“We expect the lender to have a robust account management program to monitor these [readvanceable mortgages] and manage the authorized [credit] limits where any material decline in the value of the underlying property has occurred and/or the borrower’s financial condition has changed materially,” OSFI said.

You can bank on rule changes ahead in order to mitigate this risk.

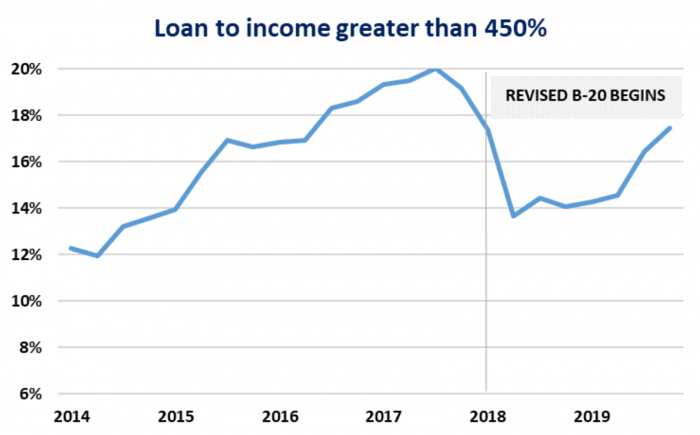

#5) Highly Indebted Borrowers Making a Comeback

“OSFI has recently observed an uptick in mortgage approvals for highly indebted borrowers,” the regulator said. Uh oh.

It’s referring in particular to mortgages that exceed 450% of a borrower’s income. The percentage of such borrowers has risen from 13.7% after the revised B-20 (stress test) rules took hold, to 17.5% last quarter.

Expect this ratio to keep climbing unless incomes somehow outpace home-price gains (don’t hold your breath on that) or regulators tighten mortgage policy yet again. Almost every key indicator points to debt accumulating faster than in prior decades. It’s no coincidence that insolvencies are spiking despite near-40-year-lows in unemployment.

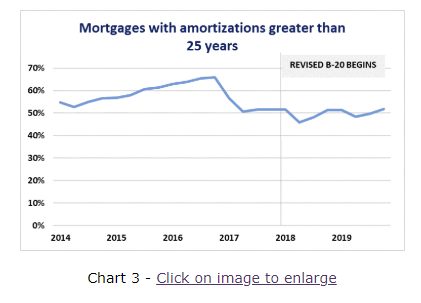

#6) Stable 30-Year Amortization Demand?

“Uninsured mortgage borrowers do not appear to be extending amortization periods to pass the stress test requirement,” OSFI said.

Source: OSFI

That may be hard to fathom for many mortgage originators. We routinely hear mortgage brokers citing anecdotal evidence of the opposite.

Regardless, OSFI’s conclusion may not reflect cause and effect. Other factors could be keeping amortizations down, potentially offsetting any amortization impact from the stress test. This includes people who:

- use lenders with more liberal debt-ratio limits in lieu of longer amortizations (some federally regulated lenders allow debt ratios above the 44% total debt service limit)

- choose non-federally regulated lenders to sidestep the stress test (stress test flunkies who use non-federally regulated lenders and get 30-year amortizations wouldn’t reflect in the above chart)

- avoid 30-year amortizations due to the amortization surcharges that started in late 2016/early 2017

- substitute HELOCs (which are interest-only) for mortgages with 30-year amortizations

One can only speculate without hard data, but one thing is clear. When a mortgage rule like B-20 slashes your borrowing power by almost 20%, you don’t just suck it up or abandon your homebuying dreams. You find a loophole, if you can. And that’s what countless borrowers are doing, something that OSFI’s data may be understating.

3 Comments

It’s exactly like you say, people are smart and will find ways to get the mortgages they need. One need only look at the growth of non-regulated private lending over the last couple of years to see this is the case. We keep hearing about the “unintended consequences” of OSFI’s rule changes. Well, I think we still don’t fully know the extent of those consequences, nor the impact they will have on the system. But time will tell all.

I think the impact of the stress on retirees should be getting more attention. People who have focused saving for retirement rather than paying down their mortgage can end up stuck with their current lender after retirement when their gross income drops. Even if their after-tax income has not dropped (possible considering pension credits and splitting), or if they have large retirement savings, retirees cannot escape the “one size fits all” B-20 rule.

To Ralph:

True. This is another reason reverse mortgages will grow fast among Canadians over 65 years old. Many would be better off in an interest only HELOC but the stress test will block that strategy, even though they are almost zero default risk.