log in

log in

“Vaccines have come too late to avoid a bleak winter,” said Capital Economics in a report last week.

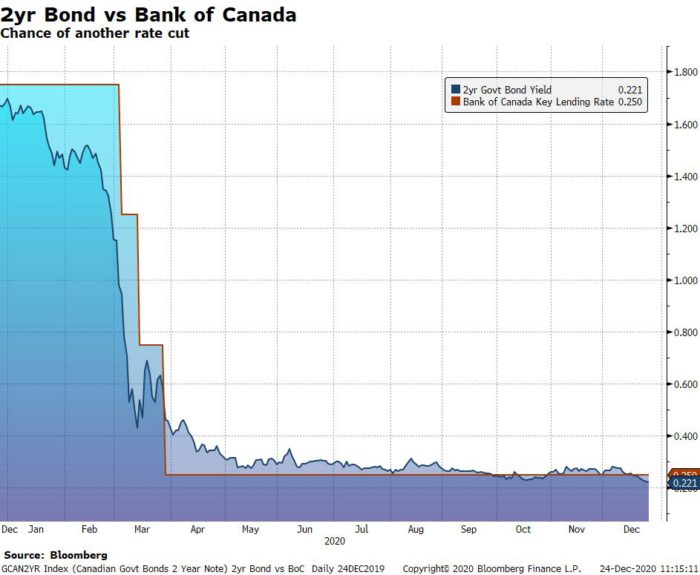

The market agrees. Canada’s two-year bond yield, often used to forecast Bank of Canada rate policy, hit a record low on Thursday.

That coincides with recent BoC comments that it could cut the overnight rate by less than the standard 25 basis points, if the recovery falters.

And falter it may. With some expecting a “grotesque” spike in C-virus cases this Christmas, inflation expectations could (temporarily) tumble. Depending on how bad the coming weeks are, it could potentially give the Bank enough cause to trim rates once more in Q1 2021.

Indeed, the BoC has been crystal clear that “…reassessing the [0.25%] effective lower bound, which would allow for the possibility of a lower—but still positive—policy rate” is an option, as Paul Beaudry, deputy BoC Governor, said in a Dec. 10 speech.

The Bank has openly discussed a potential fractional rate cut multiple times in recent weeks, leading some to think it’s setting the market up for one more rate cut in 2021.

Traders are pricing in about 10 bps of rate easing next year, according to Bloomberg. So, it’s a legit possibility that prime rate falls again, even if it’s not the most likely outcome.

By the end of 2021, however, the trend could be more bullish for mortgage rates thanks to a slew of factors noted in my Globe & Mail column this week. The bond yield spike in November was a glimpse of how willing the market is to take rates higher—once it believes that vaccinations are about to significantly reduce case counts.

For now, this wicked plague upon us will continue yielding a silver lining: lower mortgage rates near term.

Variable Rates Improve Their Lead

- The gap between fixed and variable is widening. The typical big bank discretionary 5-year variable is now 19 basis points below the 5-year fixed. That’s the widest spread since July.

- While a 19-basis-point discount from fixed rates won’t set anyone’s hair on fire, hints of another BoC cut in 2021 might drive incrementally more borrowers towards variable mortgages.

- With RBC lowering its special variable rate from 2.00% to 1.90% (prime – 0.55%) last week, all the Big 6 are now under 2% on their advertised floating rates. But that’s just their public rates. If you’re well-qualified, they’re all willing to shave at least 10-20 bps off those numbers to win your business.

- As always, shop the broker market as well. They’re up to 41 bps below mega-bank rates, depending on the type of mortgage you need.

Quick Hits

- The new BMO digital mortgage pre-approval has some pluses, but is it a game changer? I review it over at RATESDOTCA. (Story)

- “Economic slack” will “likely be absorbed sooner than central banks have assumed,” says RBC Capital Markets. As a result, it’s pulling forward its rate-hike call. “We now expect a first hike from the BoC in Q3-2022.”

- “Longer term, interest rates should go up”—Mark Carney, former head of the Bank of Canada and the Bank of England (via The Globe & Mail).

- Mortgage growth is trending at 7% annualized, according to the latest BoC data. That’s just about at its 20-year average—not bad for one of the worst recession years of all time.

- Germaphobes beware: One survey suggests that “only 19% of teller areas [in North American banks] were cleaned between customers.”

- HSBC has crushed mortgage competitors on pricing in 2020, but its mortgage volumes are still modest versus the big boys. Its latest OSFI filings show it having just $28.3B of residential mortgages on its book (plus HELOCs). That’s just 8.4% of RBC’s mortgage book, for example. But keep in mind, HSBC’s insured mortgage volumes surged 72% y/y in 2020 (to date), drastically more than any of the Big 6.

Merry Christmas / happy holidays to all!

3 Comments

Both Scotia and BMO have had branch-level discretionary 5yr variable rates at prime -1% since a couple weeks ago.

For 5yr fixed uninsured (80% LTV), Scotia quoted me 1.59% for a value (package 1) mortgage, and 1.64% for their normal STEP (package 2). Some well-qualified clients should be able to get Scotia to match CIBC’s 1.49% when requesting a rate exception from underwriting.

@Ralph

Yes, but CIBC is throwing in up to $3000 cash on the 1.49% 4Y fixed. Will Scotia match that too?

@Paul My comment was in reference to the “Variable Rates Improve Their Lead” heading. I agree with Rob that the spread between 5-year fixed and variable is around 19bps. And as you point out, 4-year fixed rates are more attractive, in particular with cash back deals. $1k on a $150k mortgage reduces the effective rate by more than 15bps on a 4yr term.