log in

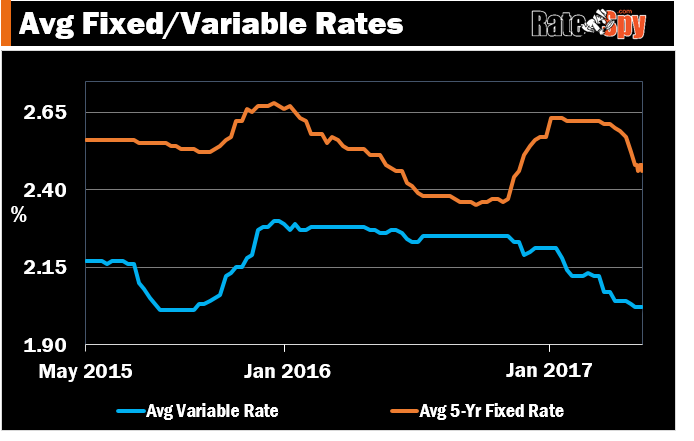

log inFixed and variable rates began the year on totally different trajectories. Fixed rates were on the way up. Variable rates were on the way down.

But in the last eight weeks, the gap between the two has conspicuously narrowed, with fixed rates falling up to 20 bps. That’s driven down the “insurance premium” borrowers pay for the security of a fixed rate.

Canada’s lowest 5-year fixed rates are now back to within 16 bps of the 1.99% psychological threshold. Of course, the lowest rates are for insured mortgages only. What else is new?

Insured mortgages are now a whopping 28 bps lower than comparable uninsured mortgages. That’s how much investors value our sovereign’s mortgage guarantee.

This gap between insured and uninsured rates has continued to widen since the Liberals:

- restricted default insurance last fall

- raised insurance costs earlier this year.

That said, we’re seeing renewed competitiveness on uninsured rates. Discounts on uninsured refinance rates have improved by 4 bps in the last month, relative to 5-year swap rates (which are a rough proxy for lenders’ base funding cost). Put another way, the pricing advantage of major banks—who don’t need to insure their mortgages—has ebbed somewhat.

Why fixed rates are falling

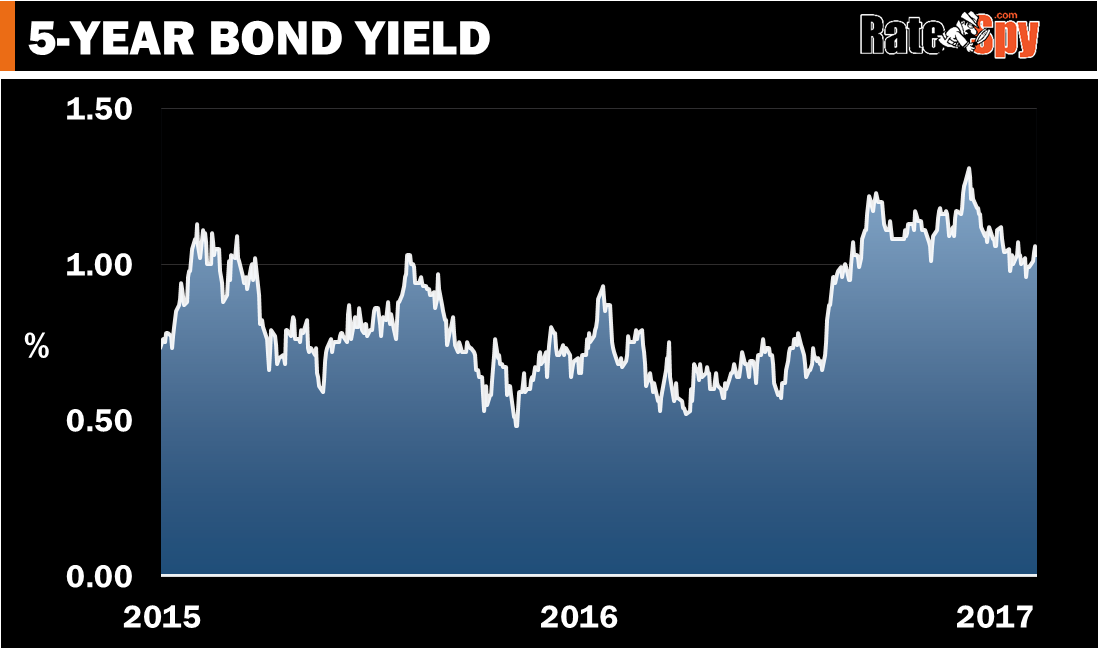

There’s no magic about it. Fixed mortgage rates have simply followed the descent in Canada’s 5-year bond yield.

The catalysts for lower rates have been a loss of faith in Trump’s economic agenda, falling oil prices and anti-inflationary economic data.

What Now

A big uptrend started last fall, but rates never ascend in a straight line. There are always pullbacks.

The question of the day is whether this rate drop is a pullback, or a directional change entirely.

Among other things, the answer will depend on the:

- power of ‘Trumponomics’ to energize America’s (and potentially Canada’s) economy

- price of oil, which strongly influences Canadian interest rates

- great unknown (is a global crisis in the wings that’ll drive down yields?)

The best thing most armchair rate observers can do is stay in their armchair and not try to decipher this randomness. Take solace that rates won’t soar, not as long as the 5-year yield stays below its 2-year high (which is 1.33% for those keeping track).

Fixed-rate Savings

All this is welcome news for mortgage shoppers stuck on a 5-year fixed. In January, Canada’s lowest 5-year fixed rate was 2.33%. Today, insured rates are back to as low as 2.15%

On a $300,000 mortgage, that’s a $2,525 savings for 5-fixed borrowers. And that’s over just one five-year term.

7 Comments

Do you think there will be any impact on the moody’s downgrade of the main banks?

https://www.moodys.com/research/Moodys-downgrades-Canadian-Banks–PR_366355

Hey Ben, It’s raised banks’ overall funding costs but it won’t have a major impact on mortgage rates or credit availability.

Welcome news for this mortgage shopper, that’s for sure! I’ve been noticing rates dropping slowly over the last few weeks and quietly wondering whether we’ll see a return to that juicy 1.99% rate.

Would conventional rates be expected to keep that roughly 28 bps buffer between their insured counterparts, or could we see that gap narrow as well?

Now that refinances are limited to 80%, uninsured mortgages should be the vast majority of new mortgage business. Keep the primary discussion on uninsured rates; the insured rates should be an aside.

Your lowest mortgage rate search still has insured rates showing up for LTV<=80%. For example DLC's 1.95% deal on 5yr variable.

Hey Ralph,

A lot of conventional mortgages are still insured.

Overall, insured mortgages comprise roughly one-third of originations, according to the Bank of Canada (http://www.bankofcanada.ca/wp-content/uploads/2016/06/fsr-june2016.pdf). So insured market share is not insignificant by any means.

As for 1.95% variable rates, there are any number of brokers offering that rate (and lower) on conventional deals.

If you only want to see variable rates that apply to conventional refinances, click “Yes” next to “Available for Refinances?”

Rob,

If 70% of mortgage originations are uninsured, that is certainly a majority. “Vast” might be a bit strong, but I’d wager that since the latest CMHC changes on March 17, close to 75% of mortgage originations are uninsured.

Regarding your rate listings, I’m searching for rates in NS. I think the problem with your database is that it may be showing rates that are just for Halifax. While the big banks will do mortgages from Clark’s Harbour to Meat Cove, some brokers have deals that are only available in larger urban centers like Halifax (and maybe Sydney). I’ve also heard of some lenders that only lend on properties that are on municipal services.

Somewhere around 67% of mortgages were insured at origination. This number will definitely rise — to what, we don’t know.

In any case, first-timers, switchers and low-ratio purchasers still need the lowest rates, which often require insurance. So the Spy will continue to provide data and commentary for insured rates.

For NS rates, please use this link: https://www.ratespy.com/best-mortgage-rates-Nova-Scotia