log in

log inCanadian rates will follow their own path. Our economy isn’t sturdy enough to track U.S. rates higher…for long.

Economists have been singing that tune for months now. And yet, Canada’s closely watched 5-year yield and its American cousin (the U.S. 5-year note) are moving together like train tracks.

U.S. & Cdn 5-year yield performance — Last 2 months. Source: MarketWatch.com

Why aren’t Canadian rates diverging more from U.S. rates? Technical factors aside, maybe the all-knowing market machine sees more Canadian growth potential than media headlines suggest.

There are two things that traders are not second-guessing right now:

- the long-standing correlation between each country’s rates, and

- the fact that U.S. prosperity could trigger Canadian inflation (which is kryptonite for bond prices and hence, bullish for rates).

The Fixed Rate Tide Keeps Rising

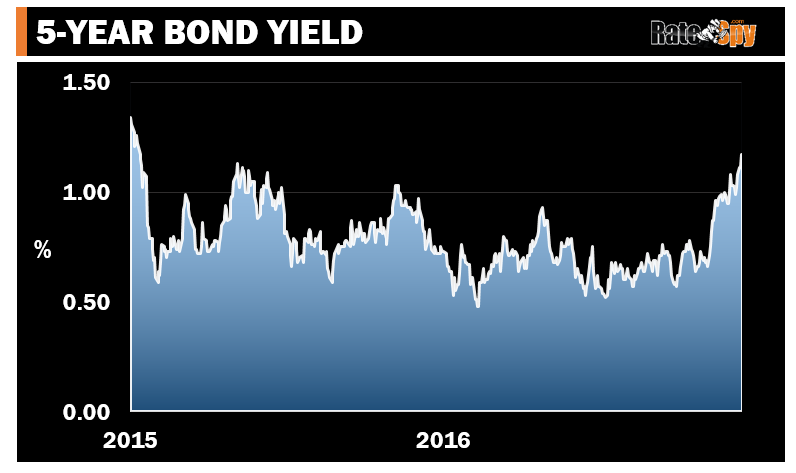

Canada’s 5-year yield, which governs fixed mortgage rates, is approaching a 19-month high.

It’s no revelation then that almost every single lender has been jacking up fixed rates. But not only are yields surging, lenders are still adjusting to the higher costs of Ottawa’s recently announced insurance restrictions and capital requirements.

It wouldn’t at all be surprising to see lenders lift rates once more before the market pauses to ponder what Trump, oil prices and Ottawa’s overactive policy-makers do next.

If you’re shopping for a mortgage today, the value zones are currently:

- Any full-featured 5-year fixed rate of 2.49% or less

- Any full-featured 2-year or 3-year fixed rate of 2.09% or less

The Variable Picture

Variables entail some rate risk in the next few years. But that’s tolerable if you’re financially secure and can find one at prime – 0.60% (2.10%) or better — especially if there’s a chance you may need to break the mortgage before maturity. (Variables have cheaper breakage penalties than most fixeds.)

People scoff when they hear suggestions that the Bank of Canada may hike next year. But if you had a dollar for every time an expert was wrong, you wouldn’t need a mortgage.

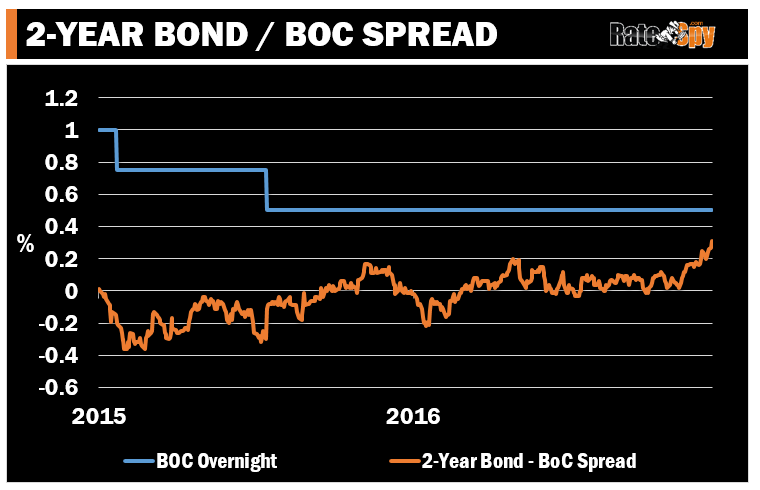

The facts stand on their own. The market is sending bullish rate signals. Witness the 2-year-GoC indicator — i.e., our 2-year government yield minus the Bank of Canada overnight rate. This “spread,” as they call it, is now 0.31%. Anything over 0.25% reflects market expectations that a future BoC rate hike is in the cards.

It makes little sense to question this and try to outsmart the market (regardless of the fact that rates may revert lower in the future). If you’re risk averse, you’re better off finding a nice cozy fixed-rate shelter to ride out the rate storm.

3 Comments

With prime – 0.65% 5yr variable mortgages now on the market, I think that’s a better option than a 5yr fixed at 2.4-2.5%. Remember the last two rate drops resulted in only 15 bp drops in prime, so two rate increases should result in just a 0.3% increase for variable-rate mortgages.

For my money I’d grab a short-term fixed under 2%. But the “better” option is always client-specific. Variables aren’t a tight fit for those with less secure income/employment, less risk tolerance and/or less financial resources. As for what prime does when the BoC raises next, a 1/4 point bump is not out of the question.

I’m in NS, and the cheapest 2yr rate on ratespy is 2.09% from True North. We have a 1yr fixed @2.04% expiring next month, and after 2 rounds of negotiating I’ve only been able to get Scotia down to 2.29% for a 2yr renewal. Aside from HSBC, the lowest rates seem to be only on insured mortgages, and there is no way to switch into an insured mortgage even if you are willing to pay the CMHC premium.

As for clients with low risk (or volatility) tolerance, they should be going for a 5yr fixed. For people with a high DSR, some lenders seem to be using the 4.64% qualifying rate even on fixed terms that are less than 5yrs, effectively limiting them to 5yr fixed mortgages.