Southbound Fixed Rates: Lender after lender has announced fixed-rate drops this week. And with Canada’s 5-year yield closing at a record low today, it’s no coincidence. It was the first time ever that our 5-year bond closed below 0.40%.

Prerequisite for Recovery: “…We need monetary stimulus to reach the ultimate borrower,” saidBoC chief Stephan Poloz today. “That, in turn, requires” easing of “posted longer-term mortgage rates” (which determine the stress test). If only the bankers pulling the strings on 5-year posted rates were listening.

Deflation Risk, Not Inflation Risk: Poloz says the hundreds of billions of dollars of support that the BoC is giving the economy is “not inflationary.”

HELOC Squeeze: Another of the biggest U.S. lenders, Wells Fargo, has banned new HELOC applications. JPMorgan did the same last week. This is highly unusual risk-averse behaviour. There’s no sign of the same happening in Canada, but some lenders are tightening HELOC requirements internally. It’s just not making headlines.

Choose Your Own Adventure:This story says home prices are immune to COVID-19. This story says home prices are about to “get hammered” by COVID-19.

11:52 a.m. Update

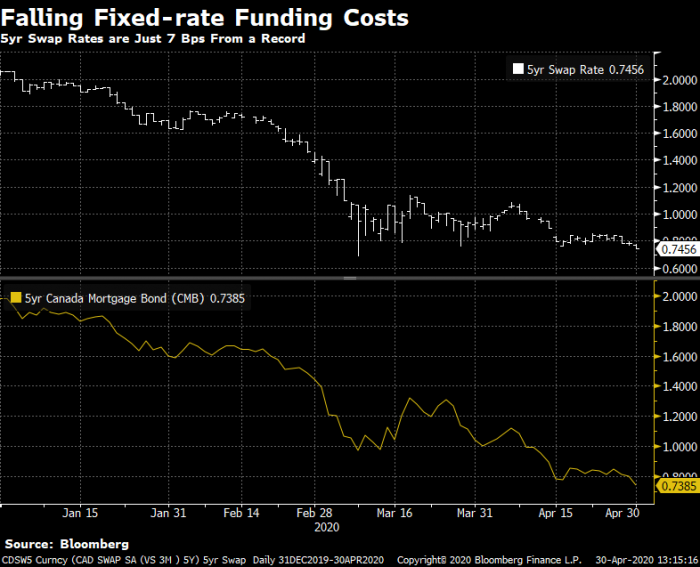

Record Seeking: One of the best indicators of near-term fixed-rate mortgage pricing is Canada’s 5-year swap rate, and it’s seemingly on a collision course with its March 9 all-time low. It’s now just 7 basis points away, suggesting further near-term fixed rate drops may be forthcoming.

Variable-rate Improvement: HSBC has become the first major lender to return to prime – 0.50% on variable rates, but only on insured mortgages so far. Here’s a summary of its new and improved rate specials:

5yr variable (high ratio): 2.34% to 1.95% (Prime – 0.50)

Tied with brokers for Canada’s lowest variable rate

5yr variable (switch): 2.40% to 2.25% (Prime – 0.20)

Rate Bearish: Business confidence has never been lower, says The Conference Board. “…Very few business leaders are expecting the economy, or their firms’ fortunes, to improve in the next six months.”

Shelled: Shell oil horrified investors today by cutting its dividend for the first time since World War II. Mortgage relevance: The news is another hint that our economic recovery (and rate recovery) won’t be quick.

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

Thanks Spy for all of your work on keeping us up to date with movements in the market.

I took your advice back in March to lock in and while it took 6 weeks to get the deal closed it did happen.

I just closed today on a new 5yr variable refi from HSBC at prime -1.11% (so effective rate of 1.34%), plus $2K cash back on closing. I even pulled some cash out to set aside an extra emergency reserve.

Use whatever analogy you want ” winter is coming” or “seven skinny calves eating seven fat calves” I believe we are in for at least a couple of rough years.

If you have an opportunity to pull some funding out of your home I would say do it now.

I know I will sleep better knowing I have extra cash in the bank and I do not have to worry about housing valuations for the next five years.

Hi Refi-Guy, 1.34% is tremendous. Nice job acting so quickly. Improving one’s liquidity picture (at a reasonable price) can provide invaluable peace of mind. I’ve heard from multiple folks who’ve made similar moves, in some cases parking prime – 1% money in a 2%+ savings account and writing off the interest.

Canada exports two-thirds of its oil production. For green energy to replace black energy as a contributor to jobs and GDP, we’d have to export two-thirds of our renewable energy. That will never happen in my opinion, not in the next decade. We’re just not making enough green energy at a low enough cost.

Green energy is still ages away from being able to sustain our lifestyle. We have a choice… either accept a lower standard of living or return to black gold. The cost of shipping just went down, as did the cost of fueling large trucks and jets and and and. The drop in the price of oil might do the exact opposite and fuel a renaissance of oil consumption (pardon the pun).

Look at oil back to 2008. The chart is a series of lower highs. There will be another dead cat bounce this year or next but don’t be fooled, the cat is dead by 2030.

Real cost of living (consumer price index) may soon be at negative 10%. Mortgage rates should then settle around the same to a crazy negative 10%. How is this possible? Well today gas is down about 30% and rents are down for some to 0 which is infinite %, many other costs will follow such as cars and houses. Countries will ban cash and bring in new digital money, this will allow banks to function as usual with negative rates.

Strangely Scotia no longer allows transferring part of HELOC ( as part of their Total Home Equity plan) to a mortgage at renewal time. Although it is only a 0.5% interest differential, it points to a tightening. They do allow the creation of a new mortgage though ( STEP allows max of 3 mges)

What’s everyone’s thoughts on where fixed 5 year mortgage rates are heading within a month? We are refinancing and have a 2.59 5year fixed but set to close May 15. I can delay it and hopefully it will go lower. Any thoughts ?

Hey Karen, Rates are in a downtrend. But even if we thought rates were going to be lower in 30 days, it would be irresponsible to suggest someone defer their closing. If your average borrower tries to speculate on rates 100 times, they’ll be wrong more than 50 times (i.e., rates will only drop a minority of the time, trending sideways or rising the majority of the time over a 30-day span).

2.59% is respectable for a 5yr fixed refi, assuming the terms are good and assuming a 5yr fixed is suitable for your needs (hope you got good advice on that). And don’t forget, refis are taking 30+ days to close at most lenders so re-applying elsewhere would reset that clock.

Re-fi Guy, I am not sure why HSBC would give you cash back when you are re-financing AND getting the best variable rate that was available at the time. From what I saw on their site and when I asked a mortgage specialist at HSBC, she was surprised too.

My mortgage renewal coming up in September 2020

I went to TD to discuss the rate and they said we can renew your mortgage with 2.6% for five years fixed but I have to sign on this Monday May 4

Or this rate is not there any more

So do you think I should go with that or wait because I still have a lot of time

Thanks

Hi Ashraf, The “you need to sign by Monday” ruse is a classic high-pressure sales technique. We see it all the time and it’s pathetic. While things can change, fixed rates are currently trending down at all Big 6 banks.

Thanks spy. We also have a clause that if rates go lower then they will lower it. However I can’t see the posted rates for RMG who the lender is so I am at the mercy of the my Broker to be honest and reduce my rate if it goes lower before we close. Hoping for June 1st but he’s trying to push for May 15 which we would prefer the later date

Hey Karen, If you don’t trust your broker he/she may be the wrong broker. In any case, ask them to confirm the exact rate for your specific product right before the closing date. Then compare it to the rate the broker secured for you. Tell the broker to quote rates *before* “commission buydowns” in each case, to ensure you’re comparing apples to apples.

@ Ashraf

It is not possible to predict future. But, there are strong signs that fix rates will go down. Look at analysis by ratespy on 5yr bond yield, swap rate and mortgage bonds which all are at at time lows.

log in

log in

20 Comments

Thanks Spy for all of your work on keeping us up to date with movements in the market.

I took your advice back in March to lock in and while it took 6 weeks to get the deal closed it did happen.

I just closed today on a new 5yr variable refi from HSBC at prime -1.11% (so effective rate of 1.34%), plus $2K cash back on closing. I even pulled some cash out to set aside an extra emergency reserve.

Use whatever analogy you want ” winter is coming” or “seven skinny calves eating seven fat calves” I believe we are in for at least a couple of rough years.

If you have an opportunity to pull some funding out of your home I would say do it now.

I know I will sleep better knowing I have extra cash in the bank and I do not have to worry about housing valuations for the next five years.

Good luck to all and stay safe.

Hi Refi-Guy, 1.34% is tremendous. Nice job acting so quickly. Improving one’s liquidity picture (at a reasonable price) can provide invaluable peace of mind. I’ve heard from multiple folks who’ve made similar moves, in some cases parking prime – 1% money in a 2%+ savings account and writing off the interest.

Shell cutting it’s dividend is more evidence that oil is on the way out and green energy is on the way in. Lot’s of opportunity for the future.

Canada exports two-thirds of its oil production. For green energy to replace black energy as a contributor to jobs and GDP, we’d have to export two-thirds of our renewable energy. That will never happen in my opinion, not in the next decade. We’re just not making enough green energy at a low enough cost.

Green energy is still ages away from being able to sustain our lifestyle. We have a choice… either accept a lower standard of living or return to black gold. The cost of shipping just went down, as did the cost of fueling large trucks and jets and and and. The drop in the price of oil might do the exact opposite and fuel a renaissance of oil consumption (pardon the pun).

Look at oil back to 2008. The chart is a series of lower highs. There will be another dead cat bounce this year or next but don’t be fooled, the cat is dead by 2030.

Real cost of living (consumer price index) may soon be at negative 10%. Mortgage rates should then settle around the same to a crazy negative 10%. How is this possible? Well today gas is down about 30% and rents are down for some to 0 which is infinite %, many other costs will follow such as cars and houses. Countries will ban cash and bring in new digital money, this will allow banks to function as usual with negative rates.

Rafi guy, what is the name of broker, could you share?

It was not a broker, it was through their HSBC website.

I contacted them back in March before the variable rate discount disappeared.

Unfortunately rates are significantly higher, the same type of mortgage I have is now at 2.25%

Now is probably the time to wait to let rates work their way down, my two cents.

Strangely Scotia no longer allows transferring part of HELOC ( as part of their Total Home Equity plan) to a mortgage at renewal time. Although it is only a 0.5% interest differential, it points to a tightening. They do allow the creation of a new mortgage though ( STEP allows max of 3 mges)

What’s everyone’s thoughts on where fixed 5 year mortgage rates are heading within a month? We are refinancing and have a 2.59 5year fixed but set to close May 15. I can delay it and hopefully it will go lower. Any thoughts ?

Hey Karen, Rates are in a downtrend. But even if we thought rates were going to be lower in 30 days, it would be irresponsible to suggest someone defer their closing. If your average borrower tries to speculate on rates 100 times, they’ll be wrong more than 50 times (i.e., rates will only drop a minority of the time, trending sideways or rising the majority of the time over a 30-day span).

2.59% is respectable for a 5yr fixed refi, assuming the terms are good and assuming a 5yr fixed is suitable for your needs (hope you got good advice on that). And don’t forget, refis are taking 30+ days to close at most lenders so re-applying elsewhere would reset that clock.

Re-fi Guy, I am not sure why HSBC would give you cash back when you are re-financing AND getting the best variable rate that was available at the time. From what I saw on their site and when I asked a mortgage specialist at HSBC, she was surprised too.

It was a switch and I jumped on the rate when I saw this article from the SPY.

https://www.ratespy.com/the-latest-mortgage-updates-031612337

I was actually in touch with a broker and HSBC, and the bank the broker was representing pulled their offer during the process.

I think I got lucky by applying early enough that the HSBC was willing to honour their rate.

If I had of waited a day or two it would not have been as favourable to me.

My mortgage renewal coming up in September 2020

I went to TD to discuss the rate and they said we can renew your mortgage with 2.6% for five years fixed but I have to sign on this Monday May 4

Or this rate is not there any more

So do you think I should go with that or wait because I still have a lot of time

Thanks

Hi Ashraf, The “you need to sign by Monday” ruse is a classic high-pressure sales technique. We see it all the time and it’s pathetic. While things can change, fixed rates are currently trending down at all Big 6 banks.

Sorry again do you think I have to wait because you think the rate goes down or take this rate now from TD?

My renewal comes on September 2020

Thanks spy. We also have a clause that if rates go lower then they will lower it. However I can’t see the posted rates for RMG who the lender is so I am at the mercy of the my Broker to be honest and reduce my rate if it goes lower before we close. Hoping for June 1st but he’s trying to push for May 15 which we would prefer the later date

Hey Karen, If you don’t trust your broker he/she may be the wrong broker. In any case, ask them to confirm the exact rate for your specific product right before the closing date. Then compare it to the rate the broker secured for you. Tell the broker to quote rates *before* “commission buydowns” in each case, to ensure you’re comparing apples to apples.

@ Ashraf

It is not possible to predict future. But, there are strong signs that fix rates will go down. Look at analysis by ratespy on 5yr bond yield, swap rate and mortgage bonds which all are at at time lows.