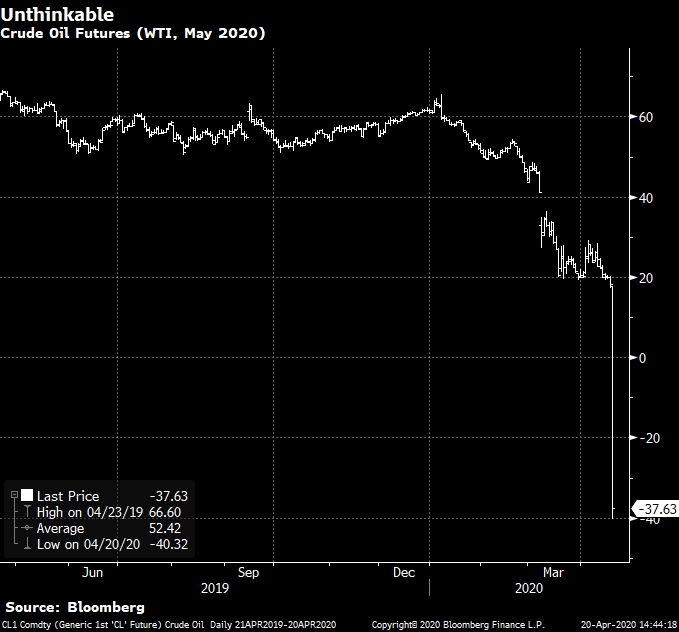

Oil Bloodbath: Crude posted its largest price decline in history today, down 300% in the May futures contract. How is it possible to fall more than 100%? Oil futures traded below $0 a barrel for the first time in history. People weren’t even willing to take a barrel of oil (for May delivery) for free. The June contract was down “only” 18%, reflecting the fact that part of today’s rout was due to technical reasons. Selling pressure has simply overwhelmed buyers as demand plummets, producers keep pumping, storage tanks are almost full and oil has no place to go. Producers worldwide are being forced to shut their wells. According to World Oil, “The last time the oil industry faced widespread shut-ins was in 1986 when Saudi Arabia also ravaged the market in a price war.” Given its typical discount to world oil, Canadian (oil sands) crude is practically worthless. Governments will likely intervene to arrange production cuts, leading to mass income losses in the sector. In the meantime, there is simply carnage.

Mortgage Impact: What do oil woes have to do with mortgages? The economic devastation playing out in Canada’s oil industry is utterly deflationary, and interest rates take their cues mainly from inflation expectations. The oil collapse, coupled with COVID-19, could potentially be one of the most rate-bearish events in Canadian history. That’s not to mention the ballooning mortgage default risk that’s facing Alberta and Saskatchewan.

Oil futures traded today at minus $40 a barrel

BoC Oil Response: Ottawa and/or the Bank of Canada may have to respond to calm markets. BoC chief Stephen Poloz is on record saying he would have cut rates up to 150 bps based on the oil shock alone, let alone because of COVID-19. And that was when oil was trading far higher. Few expect another BoC rate cut (to 0%), but few expected oil to trade below 1 cent a barrel either.

Shut Out from Help: 54% of homeowners say they’ve requested mortgage assistance from their lender during COVID, according to a new Forum Research poll. Given 60% of homeowners have mortgages, that’s the majority of people with mortgages. It’s hard to wrap one’s head around that high of a number given most people have jobs and fallback resources. We can’t help but wonder if there was an interpretation or sampling issue. But suffice it to say, a lot of people feel they’re in need of mortgage help.

Lack of Support: Just 49% of Canadians agree with the statement: “My bank (or primary financial institution) has my back during [the COVID-19] crisis.” Source: April 15 Angus Reid Poll

Potential Home Price Effects: A sampling of views on how COVID-19 may sway home prices: Rates.ca Story

Like news like this?

Join our ratespy update list and get the latest news as it happens. Unsubscribe anytime.

“Given 60% of homeowners have mortgages, that’s the majority of people with mortgages.”

I just can’t believe that is correct. So 90% of mortgage holders asked their bank for help? That simply cannot be, given most of them have not lost their jobs. Maybe the question was interpreted as whether they have thought about getting their mortgage payments reduced.

You are missing the point that deferring a mortgage at these historically low rates is just free money. So, if the bank does it, why wouldn’t I do it, specially if I am on a variable mortgage? It is like a Heloc at much lesser of a cost. And when the six month is over, pay back and reduce payments.

Mortgage deferrals aren’t free. By skipping payments on $300K mortgage you are costing yourself thousands more in interest over the amortization period. Most people can still pay their mortgage and for them it makes no sense to defer.

I’m surprised how the media is still making it appear like things can go back to normal if government shovels money at it. We won’t know until things start to be released. With courts not operating bankruptcies are being deferred. How many folks are double dipping government cheques to make their enormous mortgage and truck payments and will face reckoning when they have to pay the false claim back and pay income tax on the other? What would you say is the risk of inflation when everyone is so maxed out and high interest rates are no option?

Sorry I didn’t mean literally free and I thought it was clear. I compared with heloc and mentioned you give it back (or most of it) at the end of the six months as most lenders allow.

Let’s say you had a 500K mortgage and were on a variable 3% (prime – 0.9) with approximately 2000 per month. Your rate is now 1.5% after rate cuts. If you defer for six months, you have net 12k and if you return it at the seventh month, you must pay an additional 50 bucks (or less) for this six months and you are even with your bank.

Don’t return it and you have managed a secured low interest loan. If you were on a fixed 5 year at 3.24%, and 25 years remaining on your mortgage, you will pay 58 bucks a month for a total of 17500ish. That’s free money if you ask me.

If you have higher rate debts, use to consolidate.

If you are high income, put in rrsp and use the tax return to reduce mortgage payments. If you are not and have tfsa room, put it in tfsa. In any case, I bet that anything you buy in big tech stocks will return way way more long term.

True, most people can but at these rates, I will always get that low interest loan and put it to work. Everyone is different though.

Add to that the fact that this may end up being much worse and some people that can pay now, may not be able to do that if things get worse. Banks won’t let you defer forever. For 60 bucks, it just makes sense to keep that money as reserve if the worst comes…

The other fishy thing about the survey is the 46% that say they were denied assistance.

My wife called TD to get a deferral on our primary residence mortgage, and other than the week wait for a callback, it was easy. There were no qualification rules; if you asked for it, and understood it was extending your amortization, you got it.

We didn’t need the deferral, but we had a couple grand left on a uLoC at 4.2%, so it’s simple math when the mortgage is < 3%.

Ralph – Deferrals don’t extend the amortization. The payment is increased after deferral to get amortization back on track. The payment change takes effect at renewal or sooner.

log in

log in

12 Comments

The June contract could also go to zero according to Bank of America today.

“Given 60% of homeowners have mortgages, that’s the majority of people with mortgages.”

I just can’t believe that is correct. So 90% of mortgage holders asked their bank for help? That simply cannot be, given most of them have not lost their jobs. Maybe the question was interpreted as whether they have thought about getting their mortgage payments reduced.

Yep, like we say, we’re having a hard time reconciling this one too.

The exact question asked was:

“Did you receive any mortgage assistance, such as a payment deferral, or some other help, from your financial institution?”

Only homeowners were asked this question. According to Forum Research, the 890 respondents answered as follows:

8% — “Yes, received assistance”

46% — “No, asked for assistance but was denied”

43% — “No, did not ask for assistance”

4% — “Prefer not to say”

Thanks. I simply don’t believe the results are representative. Maybe this is that 1 time out of 20 🙂

You are missing the point that deferring a mortgage at these historically low rates is just free money. So, if the bank does it, why wouldn’t I do it, specially if I am on a variable mortgage? It is like a Heloc at much lesser of a cost. And when the six month is over, pay back and reduce payments.

Mortgage deferrals aren’t free. By skipping payments on $300K mortgage you are costing yourself thousands more in interest over the amortization period. Most people can still pay their mortgage and for them it makes no sense to defer.

I’m surprised how the media is still making it appear like things can go back to normal if government shovels money at it. We won’t know until things start to be released. With courts not operating bankruptcies are being deferred. How many folks are double dipping government cheques to make their enormous mortgage and truck payments and will face reckoning when they have to pay the false claim back and pay income tax on the other? What would you say is the risk of inflation when everyone is so maxed out and high interest rates are no option?

Sorry I didn’t mean literally free and I thought it was clear. I compared with heloc and mentioned you give it back (or most of it) at the end of the six months as most lenders allow.

Let’s say you had a 500K mortgage and were on a variable 3% (prime – 0.9) with approximately 2000 per month. Your rate is now 1.5% after rate cuts. If you defer for six months, you have net 12k and if you return it at the seventh month, you must pay an additional 50 bucks (or less) for this six months and you are even with your bank.

Don’t return it and you have managed a secured low interest loan. If you were on a fixed 5 year at 3.24%, and 25 years remaining on your mortgage, you will pay 58 bucks a month for a total of 17500ish. That’s free money if you ask me.

If you have higher rate debts, use to consolidate.

If you are high income, put in rrsp and use the tax return to reduce mortgage payments. If you are not and have tfsa room, put it in tfsa. In any case, I bet that anything you buy in big tech stocks will return way way more long term.

Trump will probably tariff Saudi oil to prop up prices.

True, most people can but at these rates, I will always get that low interest loan and put it to work. Everyone is different though.

Add to that the fact that this may end up being much worse and some people that can pay now, may not be able to do that if things get worse. Banks won’t let you defer forever. For 60 bucks, it just makes sense to keep that money as reserve if the worst comes…

The other fishy thing about the survey is the 46% that say they were denied assistance.

My wife called TD to get a deferral on our primary residence mortgage, and other than the week wait for a callback, it was easy. There were no qualification rules; if you asked for it, and understood it was extending your amortization, you got it.

We didn’t need the deferral, but we had a couple grand left on a uLoC at 4.2%, so it’s simple math when the mortgage is < 3%.

Ralph – Deferrals don’t extend the amortization. The payment is increased after deferral to get amortization back on track. The payment change takes effect at renewal or sooner.