log in

log in

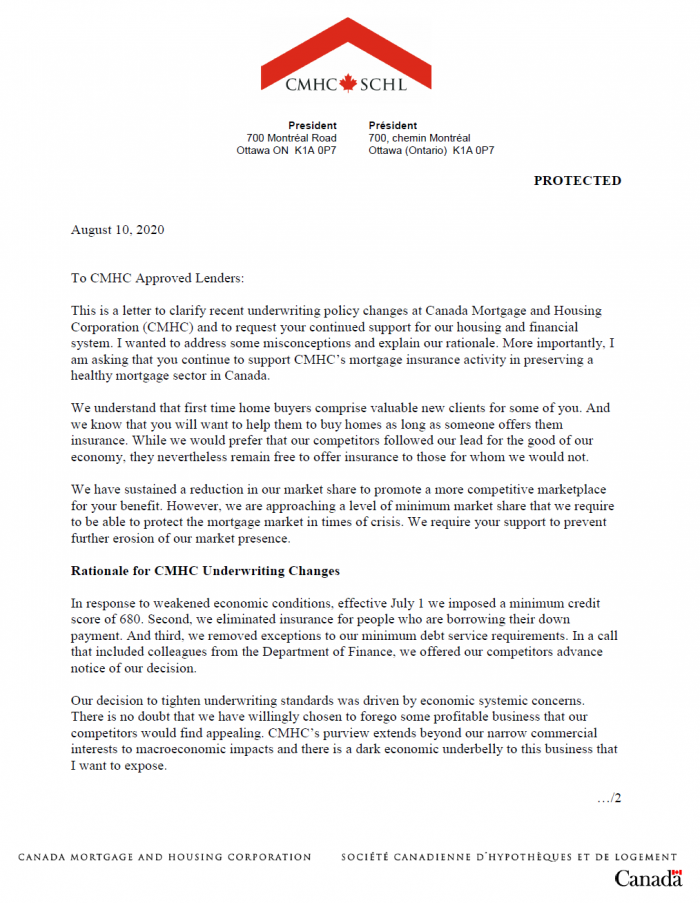

Well, you don’t see this every day: The head of Canada’s housing agency seemingly guilting lenders into sending him business and tightening mortgage lending.

In a letter to the industry originally leaked to Bloomberg (see below), CMHC CEO Evan Siddall chided and accused mortgage lenders of:

- short-sightedly sending too much business to CMHC’s competitors

- creating a “very significant drag” on the economy

- helping “people buy homes with negative equity”

- exposing “too many people to foreclosure”

- putting “short-term profitability” ahead of the country

- having a “dark…underbelly” that needs to be exposed.

These are alarming charges…for those who don’t know the backstory.

It’s a story that all starts with CMHC’s decision to stop lending to certain types of borrowers, mainly borrowers with higher-than-average debt loads.

Its competitors refused to follow CMHC’s lead, arguing that those borrowers are good credit risks with good income prospects.

That brings us to Siddall’s missive above. It was a divisive letter that never should have been sent in its current form, for at least seven reasons:

- The Letter Overlooked the #1 Cause of High Debt Ratios: Inadequate Supply Leading to High Home Prices

- Housing Canadians is CMHC’s job, and objectively speaking, its top leadership has dropped that ball. From the turn of the millennium we’ve had the same problem: not enough middle-class homes within a commute of major employment hubs. CMHC has begun some great work to house underprivileged Canadians with its $55-billion National Housing Strategy, but it’s too little too late for middle-income families. Years after the supply problem became apparent, families are still left house-poor, overpaying for the shelter they need to survive. Whether it’s a lack of strategic builder incentives, uncoordinated urban planning or insufficient prioritization of high-speed commuter rail, the agency’s inability to rally other arms of government and yield results is costing Canadians every day. While CMHC’s incredibly dedicated and talented underwriting team, securitization team, research teams, media team and social housing teams serve Canadians well, its top leadership has failed in this essential mandate.

- The Letter Ignored the Stress Test

- The elevated debt-service ratios Siddall cites are elevated largely on paper. For years, lenders stress tested 5-year fixed mortgages based on the actual rate people pay and time-tested debt-ratio limits. In 2016 and 2018, that changed and regulators forced people to prove they can afford payments at much higher rates. That was a good idea in principle, despite officials admitting to choosing the wrong qualification rate. What the stress test did, however, was skew reality because people could actually afford much more than what regulators were allowing them to borrow.

- That brings us to CMHC’s July 1 ban on borrowers with gross debt service (GDS) ratios above 35%. (“GDS ratio” refers to your housing expenses divided by your gross income). Someone with a 39% GDS on paper really has a true GDS as low as 31%, based on actual mortgage rates at origination. Today, the minimum stress test rate is a whopping 2.80 percentage points higher than real 5-year fixed rates. That means CMHC’s reduction in GDS limits actually forces its borrowers to have “true” GDS ratios well under 29%, an excessively conservative policy that constricts homebuying, which in turn constricts economic consumption and jobs.

- Because of point #1 above, sub-29% true GDS ratios are simply no longer realistic. Housing is just too expensive. There’s a reason 30-35% of Genworth’s new insurance written in Q2 had a GDS ratio over 35% and/or a TDS ratio over 42%. People are that leveraged (on paper) not because they want to be, but because they have no choice.

- And now such borrowers will have even fewer options. Thanks to CMHC’s pullout, private insurers are getting flooded with high GDS/TDS deals. As a result, privates are getting more selective and their approval rates for these customers are dropping. This brings us to the next point.

- If Lenders Do What He Says, Renters Suffer

- People can’t live on the street. For that simple reason, “Making it harder or more costly to own does not decrease overall housing demand,” points out True North Mortgage CEO Dan Eisner. “It just makes more people into renters.” Hold rental supply constant and add rental demand and guess what happens? Unless you adjust supply, “Housing prices are driven by the number of people looking for a place to live, not the number of people looking to buy.”

- Mr. Siddall is justly concerned that people are spending too much money on housing and that’ll eat into their consumption of other goods. We couldn’t agree more. But almost half of Toronto renters spend more on rent than CMHC guidelines allow them to spend on home ownership. Siddall appears to be saying it’s okay to push up rents and “slow future consumption,” but it’s not okay to maintain mortgage access if that slows consumption.

- The Letter Assumes No Accountability

- Oligopolists concerned about market share are ill-advised to unilaterally institute policy changes that defy consumer demand. And if they do, they better be darned well sure that competitors follow. Siddall appears to have badly miscalculated:

A) private insurers’ willingness to follow his lead, and

B) lenders’ desire to support private insurers. - Not only are lenders now sending all their non-CMHC compliant mortgages to Genworth and Canada Guaranty, they’re sending “less risky” business (as Siddall puts it) as well. They’re doing this because:

- there is legitimate consumer need

- they appreciate private insurers’ willingness to use common sense underwriting

- the private insurers may be encouraging them to send low-risk business to help keep their books balanced. Can’t blame them for that.

- CMHC’s market share has plunged under Siddall’s watch. Its latest plan shows it targeting up to 50% market share, but we’d be surprised if it held more than a third of the market now. Not that long ago it approached almost 90%, which reminds us of Tom Mulcair’s famous 2012 question, “Can the Finance Minister inform…all Canadians, why he wants to dismantle a 60-year success story at CMHC?”

- Given its new self-imposed restrictions, CMHC will now be overly concentrated in smaller, less liquid real estate markets — given debt ratios are lower in those markets. That’s a whole other taxpayer risk — particularly if the economy and home prices head south, as CMHC is forecasting. CMHC’s sole shareholder (the taxpayer) is left holding the bag for under-calculated decision-making that’s created a less diversified and far less profitable crown corporation.

- Oligopolists concerned about market share are ill-advised to unilaterally institute policy changes that defy consumer demand. And if they do, they better be darned well sure that competitors follow. Siddall appears to have badly miscalculated:

- The Letter Was a Weakly Argued Case

- One of Siddall’s central arguments is that CMHC needs to have 40-50% market share so it can “scale up quickly” if private insurers pull back from the market in an economic shock. The implication is that private insurers would head for the hills if home prices were diving. That assertion was unsupported in his letter.

- The reality is, private insurers have grown their participation despite the deepest recession of all time. And, if Ottawa fights future recessions like it did this one (with hundreds of billions in consumer and business aid), there’s even less reason for private insurers to cut back their presence.

- CMHC, whose very job as a crown corp. is to “take one for the team” (the team being our country), retains the ability to eat into its profit and over-staff if it feels that’s necessary for systemic stability. If it doesn’t want this obligation, perhaps it should forgo its government-bestowed competitive advantages and privatize.

- As for the important housing support that CMHC provides during crises (like its recent Insured Mortgage Purchase Program), those programs can easily be government funded regardless of CMHC’s market share.

- The Letter Seemed a Mite Bit Inconsistent

- For years, policy-makers have told us that mortgage risk must shift from the taxpayer to private companies with less government backing. Now they get their wish and they want to roll it back.

- The Letter Undermined Confidence in Canada’s Financial System

- When investors get scared for no good reason, it costs all Canadians money, homeowners or otherwise. Investors worried about our outlook pay less for Canadian bonds and businesses (foreign and domestic) invest less in our economy. That drives borrowing costs higher, limits lending and restricts job growth. If Mr. Siddall is going to yell “fire,” people are going to run, so there better darn well be a fire.

To lead an entire industry, you need credibility. Siddall’s constant unfounded charges that the industry facilitates “excessive borrowing” paints lenders and insurers as profit-hungry robber barons who couldn’t care less about doing the right thing for the country. That’s not the most endearing or effective management style. Lenders don’t speak up because they fear what Siddall can do to their business. But unless you’re Genghis Khan, you can’t lead by fear.

Mr. Siddall’s letter is replete with omission of fact and context. We, like the rest of the industry, support a safer mortgage market. In fact, we support policies that should have already been taken to reduce borrower risk, but haven’t been. What we don’t support is this illogical crusade against homeownership that does nothing to correct the supply/demand imbalance that’s fueling excessive debt in the first place.

Siddall admitted that “CMHC cannot stop” lenders and insurers from approving the insured mortgages he declines. That’s why, this author believes, he CC’d top policy-makers on this letter. His hope may be that regulators “have his back” and force the rest of the industry to adopt his changes—once again proving him “right.”

But doing that would compel the qualified borrowers he no longer wants into renting or higher-cost lending. That’s a problem. Whether someone rents or buys should remain a personal decision hinging on their qualifications and needs.

If the likes of Siddall are going to manipulate the market, do it to solve one of Canada’s most urgent economic crises: the imbalance in middle-class housing stock. Economists almost unanimously support this.

As for manipulating general debt ratio limits in our already conservative “stress test” era—not only does that flout the law of diminishing returns, it creates a host of other economic imbalances.

Industry leaders confiding in me today were united on two fronts: that Mr. Siddall has lost their trust with such reckless assertions, and by virtue of that, has now officially overstayed his welcome in the Canadian mortgage market.

Viewpoint stories are opinion pieces. They solely reflect the author’s perspectives and not the operators of RateSpy.com.

28 Comments

Australia has a contract plus 2.5% “stress test”. Seems pretty close to what we’ve got no? We’re not out to lunch are we? In fact before 2019 the Australian regulator (APRA) had a minimum 7% floor rate for debt serviceability. The fact that we used to allow (and still do!) allow people to qualify at the contract rate was, IMO, rash.

We as a country give plenty of support to housing and I think it’s prudent to pull some of that stimulus back. And FYI, there is no affordability crisis in Calgary, Saskatoon, Edmonton, Winnipeg and Halifax (among thousands of other Canadian cities).

Nice article.

Another reason:

8. It’s completely ineffectual. Evan should ask Jim Flaherty how well it works to chide the big banks not to follow the market. Evan is saying they lost massive market share by tightening lending and his advice is to follow their lead? Not much of an argument for a lender/insurer with shareholders.

Used to have a lot of respect for Evan but no longer. The forecast was badly done, and now this, and he’s coming unhinged on Twitter at perfectly reasonable criticism. Not sure where they get the nerve to chastise lenders for allowing 5% down with a 4% insurance premium when that’s what they allow! If they want to beef up the minimums then they should do that and skip the theatre

In your view, what is the maximum that a household should spend on housing costs and other debts, as a percentage of their income? It sounds like you are suggesting that even the limits that the private insurers are using are too conservative. Are you suggesting that these limits be increased on the basis that Canadians can “afford” to spend a greater portion of their income on debts? I can’t imagine ever spending more than 30% of my gross income on housing – and still go on a vacation, eat well, save for my kids education, put them in hockey etc. I wonder if you can write your next article outlining the impact of these truly harmful practices of realtors in Toronto and these blind auctions resulting in sale prices way over asking. Are you willing to take on Hudak for the harmful tactics of his members with the same passion that you have demonstrated in taking on cmhc?

Hi David,

“What is the maximum that a household should spend on housing costs and other debts, as a percentage of their income?”

Unfortunately that question can’t be answered in isolation. If I’m a new doctor earning $8,000 a month today but $20,000 a month soon after, is it not safe to be somewhat more liberal on the TDS ratio at origination?

The answer will also differ for someone who’s got ample liquid assets versus someone with few fallback resources. This is what underwriting is all about, factoring in each borrower’s unique circumstances to assess debt serviceability.

“It sounds like you are suggesting that even the limits that the private insurers are using are too conservative.”

In some cases they are. Good luck justifying a 280 bps higher qualifying rate on a 10-year term, for example.

“I can’t imagine ever spending more than 30% of my gross income on housing”

Apparently you’re not the average Torontonian or Vancouverite. 🙂

“I wonder if you can write your next article outlining the impact of these truly harmful practices of realtors in Toronto and these blind auctions resulting in sale prices way over asking.”

People hate being on the buying end of a blind bidding transaction.

People love being on the selling end of a blind bidding transaction.

So who do you fight for? It seems someone arbitrary to pick one side over the other as the seller of any asset has the right to maximize their gains. For many people, a house is the only real asset they’ve got.

The reality is that it’s just as easy to overpay in a chaotic open auction. Buyers will ultimately reach their terminal bid regardless, simply because they know there’s competition to beat and they can submit multiple bids.

The stress test is arguably controversial. It’s intention was to determine the ability for a borrower to handle higher interest rates- which never have happened. And for the next five years, won’t happen. It’s a fail. If they insist on a stress test, it should be 1% above contract rate, or the contract rate for terms higher than 5 years.

If the Nations insurer wants to really understand a true GDS it should factor in realistic heating costs (not $75-100 that some brokers use to get an approval), homeowner insurance, and 100% of condo fees. All three sundry costs are required to get a mortgage but yet we discount them to get an approval.

If the GDS exception is kept under 35% then those with good credit and good income/job stability are penalized for no reason. Mortgage defaults in Canada have been historically low. And the threat of interest rate creep has been kept at bay.

Canada is a global dependant economy. Factors outside of Canada influence our rates.

It may get a lot worse. I hear former OSFI Assistant Superintendent Carolyn Rogers is being considered for Evan’s position.

@Pizderi

Newsflash: We’re in a recession. Housing is one of few sectors that’s working right now. Pulling back housing support during a down cycle is called pro-cyclical. It makes recessions worse.

Calgary, Saskatoon, Edmonton, Winnipeg and Halifax don’t matter. CMHC is making policies for places like Toronto, Vancouver, Ottawa, Montreal and Victoria.

There is nothing wrong with qualifying at contract rate if the term is long enough. People qualified at contract for decades and somehow we’ve survived. It is crazy that people getting a 10 year fixed have to qualify at a higher rate. After 10 years they have 35% equity, even if home prices don’t rise $1

You know I’d really like to see Mr. Siddall dropped into a situation where he as to find a home to live in with all these new rules with a middle income salary…

So let me get this straight. Siddall wants people with higher GDS & TDS to rent so they can consume more? Maybe Siddall should go back to economics school. Last I checked home buyers make 2-3 times the shelter-related expenditures of renters.

@David is spot on.

Sounds like RateSpy is part of the dark economic underbelly.

Rapacious realtors and shady mortgage lenders low on ethics.

Evan Siddall is spot on.

@Hellno you just made me literally say the words

“Oh.

My.

God”

and release a huge sigh.

Say it ain’t so.

RBC’s prior CEO calls Evan’s letter “extreme and alarmist.”

https://www.bnnbloomberg.ca/video/i-hope-cmhc-is-not-correct-on-risky-mortgage-lending-former-rbc-ceo-nixon~2013160

He says banks may cave and send CMHC more business “at the margin” because of this letter.

Excellent comments regarding Siddall’s recent letter. I propose a more logical remedy with respect to the now chaotic CMHC. Private Industry Leaders electing-in his replacement who would periodically testify before Federal government law-makers.

Just pick random 1000 approved mortgage applications from last 6 months, CMHC letter will start making sense to you all .. The magnitude of fraud will blow your mind. approvals on fake jobs, imaginary paperwork, unproven source of fund etc will explain how people can afford 3-4 houses. The high prices are not demand / supply case.. Its purely driven by greed and the magic realtors / brokers do. Prices are going up because lenders are approving easily just for their own short term benefits.. This will all end up on a pretty bad note sooner or later…

@Johny – Where do you get your mortgages? The local cheque cashing storefront? My cousin Vinnie?

Contrary to your unfounded claims – I’ve only had very stringent mortgaging apps and the process for most took much longer than I had hoped for. I highly doubt this is still happening after the HomeTrust fiasco and Laurentian Bank’s spanking by the market after they sold off a package of mortgages that weren’t thoroughly checked – which also by the way had a lower rate of issues than what’s posted by other banks LOL. Siddall is the definition of a hypocrite. For years he led the organization that enabled the market as it currently is, and now he’s going to tell others what to do and not do? Give me a break.

Looks like Evan Siddall has gone Full Monty and decided to let it all hang out and go down swinging.

Sounds more like like a mad-man by cryptically alluding to “dark underbellies” and invoking incoherent wartime analogies. No?

Thanks all for the support and feedback. Much appreciated.

The fact that Siddall spouts all homebuyers with 5% down as debt laden risks is not borne out anywhere in the past delinquency record of CMHC which has been less than 1/2 of 1%.

From first quarter 2020 CMHC report:

Delinquency rates are steady across Canada at 0.29%. Montreal continues to trend lower, below the national average. Toronto and Vancouver maintain a flat rate much lower than national average, at 0.11% and 0.13%, respectively.

Similarly, delinquency rates are relatively flat across most age cohorts. The exception is the 25 – 34 age group — usually young first time homebuyers. Their delinquency rates continue to trend lower to the lowest of any cohort, at 0.24%.” -Wow -first time buyers are the lowest % delinquency cohort!!

“The share of mortgages held by consumers with high credit scores (700+) continues to trend higher. It represents 86.23% of outstanding loans, as well as 85.52% of new mortgage loans. The number of mortgage loans outstanding continue to be held by decreasingly risky consumers.”

Decreasing risky consumers!!!

Also dismissed is that CMHC had been a government cash cow for years with money flowing into the general government coffers.

This from May 2020:

“Generated revenues and government funding of $4.7 billion and a net income of nearly $1.6 billion. Declared more than $2 billion in dividends, payable to our shareholder, the Government of Canada. We hold capital for these activities in line with our risk profile and with regulatory capital requirements.” May 5, 2020

So what is he saying? If they hold capital in line with risk as of end of March, has the situation changed that drastically in 4 months and where did that capital go?

Now since they are seeing less of the market, perhaps the potential profit dip has Treasury concerned with all the Covid money going out the door and Siddall is trying to justify his position and trying to make his predictions a self fulfilling prophecy by creating alarm within the market?? Where are these dark underbellies? Where is the war? I think he’s gone a little Trump!

Isn’t Siddall’s term up at the end of the year?

Hey Ralph, Yep.

It seems that CMHC changes mortgage rules to slow the skyrocketing house prices.

The house prices rise because of lack of supply and increased demand. Stop changing the mortgage guidelines and start changing the home purchasing rules. How many properties in the large urban areas are being purchased by foreign investors with no mortgages? if we limit foreign buyers then we increase the supply for domestic buyers. Just my view point.

In contrast to CMHC, Genworth noted in their recent Q2 presentation that their business was booming – transactional insurance (i.e. policies paid directly by home owners) was up year-over-year by 50% in June and 75% in July.

Their new Q2 business also came with an average premium of 3.49% down from 3.52% in Q2 2019. In other words their new business is slightly less risky than the old. Genworth is definitely doing more than simply picking up CMHC’s rejects.

I can’t say I’m a fan of Mr. Siddall’s communication style but you have to admire some-one who sticks to his principles. He also has bigger problems to cope with.

For the last few years CMHC has been conducting an increasing share of their consumer fronting business in Quebec. In the first quarter of 2020 that province accounted for 29.5% of new transactional policies on a dollar value basis (versus 30.1% in much larger Ontario) and around 38% of new transaction policies on a per unit basis (versus around 21% in Ontario’s). If Genworth and Canada Guaranty have acquired a disproportionate share of their new windfall business in Ontario, CMHC’s exposure to Quebec’s economy may now be way past Mr. Siddall’s comfort level.

Such a position is unsustainable. If this scenario is correct, then sooner or later CMHC will need to cut back on new business from Quebec in order to adequately diversify their portfolio. Such an act could have serious economic and political implications if Genworth and Canada Guaranty are unwilling to build up their Quebec business to offset CMHC’s withdrawal.

Thanks for that colour, Ken. Haven’t had a chance to dive into the numbers to confirm but it would be an interesting twist if true.

@Avner, ok so with the current avg prices in GTA, you saying avg income of everyone in Toronto is in 100K’s ? oh yeah… and ppl owning 5-6 houses cuz many of us are millionaires ?

Wake up my friend.. don’t act like Alice in the wonderland… Without the “special magic”, no one would qualify for such hefty loans.. If lenders are told to pull up income from CRA , no one will ever get approved. Its not supply or demand issue. Its issue of greed, when everyone wants to own 5-6 houses cuz magicians are there to help them.. you can never fill the supply.

The stress test is bs. If they are going to speculate on interest rates then let’s speculate on incomes and property values.

Hey Mark, At contract rate + 300 bps, I have to agree with you.

Why can’t we have a policy that prioritizes a Canadian buyer over a foreign buyer? Or better yet, prioritize the Canadian buyer who actually plans to live in the home. (and not by having them borrow from their retirement savings!)

Hey Angela,

The fact is, a majority of Canadians share your sentiments, according to more than one survey I’ve seen.

On the latter point, Canada need rental supply. We need individual landlord owners.