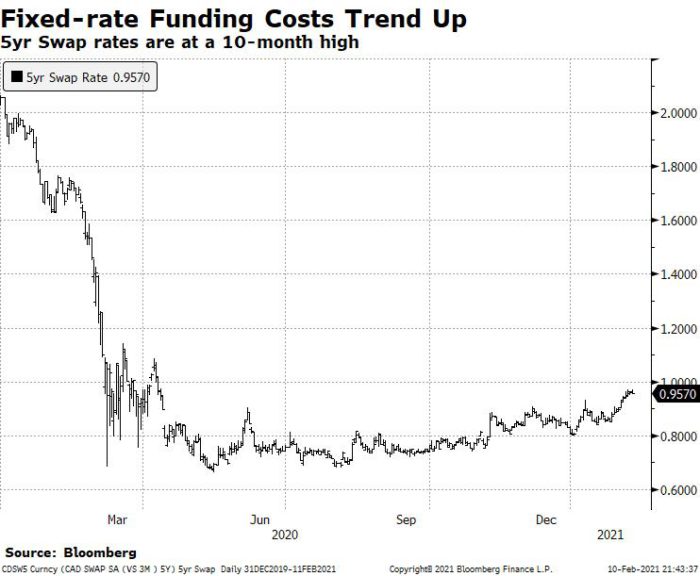

It’s not getting any cheaper for banks to fund a fixed-rate mortgage. In fact, Canada’s 5-year swap rate, a common measure of 5-year funding costs at the big banks, is running at a 10-month high.

Yet, still we’re seeing lenders trim 5-year fixed rates as the cut-throat spring market approaches. RBC chopped its 5-year fixed by 18 bps last week. And on Wednesday, CIBC trimmed its advertised uninsured 5-year fixed to 1.99%, tying TD for the lowest of the major banks.

How much longer banks are willing to accept shrinking spreads (profit margins) is anyone’s guess. They still have billions in government-backed liquidity that they have to put to work, and mortgages are a nice, safe asset class. Moreover, “We are basically in a recession,” CIBC economist Ben Tal told the Post on Tuesday. Given that, and relentless competition, banks can barely afford to raise their asking prices on mortgages.

Meanwhile, 5-year forward rates are now over one percentage point above 5-year bond yields. That’s the biggest gap since May 2017, and confirmation that rates are likely headed higher, so thinks the market.

All that is to say, while this may not be the last hurrah for 5-year fixed rates, there are fewer and fewer hurrahs left.

This & That

CIBC dropped its 5-year variable rate by 19 bps on Wednesday to 1.69%, the lowest advertised floating rate of any Big 6 bank. The move follows a similar 15-bps RBC cut last week. Expect banks to push variable rates hard, right before 5-year fixed rates lift off.

Given movement in 5 yrs (~ 49bps) from your last post and now 5 yr swap spreads here, what would you recommend for someone whose 5 yr fixed mortgage (2.59%) is up for renewal at the start of april, *but* will be moving in the summer at some point?

– Renew with a 5 yr, no prepayment penalty paid now, and negotiate in portability? (could be an issue as our current mortgage is insured and we may potentially need > $1MM / uninsured). Even without portability the prepayment charge on a 5 yr fixed even broken early wouldn’t be much with rates where they’re trending (up), correct?

– Fully open HELOC (which would mean paying a prepayment penalty now), layering in a 90 / 120d preapproval on a 5 yr fixed to hopefully cover the next purchase?

– Go 1 yr fixed?

The idea of course is to get a good all in borrowing cost (i.e. avoid unnecessary prepayment charges)

Hi Neil, It’s unlikely that a borrower would get a great deal negotiating an uninsured port and increase rate, after just locking into a new 5-year insured term. The existing lender has too much leverage and (if a non-bank lender) much less favourable funding costs on uninsured money.

For someone needing financing for just 3-4 months, the better play would be getting the cheapest possible open term with the lowest possible rate and fees. Then get a good rate hold 90- to 120-days before moving day.

Good afternoon, my 5 year BMO fixed mortgage term is up July 1st 2021. I noticed I can secure a 10-year fixed rate with Tangerine on their website (an eye popping 2.14% this would be my last as I only have 10 years left on my mortgage) however if I secure now it only secures until Jun 11th.

Should I secure the 10-year 2.14% fixed rate now and worst case scenario on Jun 10th break my BMO mortgage with 3 weeks left or hope nothing changes until March 1st and lock in the rate with Tangerine at that point?

Hi David, BMO should charge you just the remaining interest when breaking with three weeks to maturity (definitely call BMO to confirm that).

Then get a 120-day rate hold from Tangerine. Ask Tangerine to reset the rate hold once you’re 120 days from renewal if the 2.14% is still available then — in which case you can switch lenders at maturity with no penalty.

Hi David,

I have a CIBC 5 year fixed at 3.44% 25 yr amort due Oct 2023.

The penalty is large 11,593. They are offering $2500 off the penalty and 1.79% for 5 yr fixed 20 amort.

Not sure what to do? I have it on hold for 2 weeks.

Wait to see about rates?

log in

log in

6 Comments

Hi Rob (Spy),

Given movement in 5 yrs (~ 49bps) from your last post and now 5 yr swap spreads here, what would you recommend for someone whose 5 yr fixed mortgage (2.59%) is up for renewal at the start of april, *but* will be moving in the summer at some point?

– Renew with a 5 yr, no prepayment penalty paid now, and negotiate in portability? (could be an issue as our current mortgage is insured and we may potentially need > $1MM / uninsured). Even without portability the prepayment charge on a 5 yr fixed even broken early wouldn’t be much with rates where they’re trending (up), correct?

– Fully open HELOC (which would mean paying a prepayment penalty now), layering in a 90 / 120d preapproval on a 5 yr fixed to hopefully cover the next purchase?

– Go 1 yr fixed?

The idea of course is to get a good all in borrowing cost (i.e. avoid unnecessary prepayment charges)

Many thanks!!

Hi Neil, It’s unlikely that a borrower would get a great deal negotiating an uninsured port and increase rate, after just locking into a new 5-year insured term. The existing lender has too much leverage and (if a non-bank lender) much less favourable funding costs on uninsured money.

For someone needing financing for just 3-4 months, the better play would be getting the cheapest possible open term with the lowest possible rate and fees. Then get a good rate hold 90- to 120-days before moving day.

Good afternoon, my 5 year BMO fixed mortgage term is up July 1st 2021. I noticed I can secure a 10-year fixed rate with Tangerine on their website (an eye popping 2.14% this would be my last as I only have 10 years left on my mortgage) however if I secure now it only secures until Jun 11th.

Should I secure the 10-year 2.14% fixed rate now and worst case scenario on Jun 10th break my BMO mortgage with 3 weeks left or hope nothing changes until March 1st and lock in the rate with Tangerine at that point?

Thoughts?

Hi David, BMO should charge you just the remaining interest when breaking with three weeks to maturity (definitely call BMO to confirm that).

Then get a 120-day rate hold from Tangerine. Ask Tangerine to reset the rate hold once you’re 120 days from renewal if the 2.14% is still available then — in which case you can switch lenders at maturity with no penalty.

Hi David,

I have a CIBC 5 year fixed at 3.44% 25 yr amort due Oct 2023.

The penalty is large 11,593. They are offering $2500 off the penalty and 1.79% for 5 yr fixed 20 amort.

Not sure what to do? I have it on hold for 2 weeks.

Wait to see about rates?

Hi David

To add to above. I could go to another institution for a rate of 1.69 for 5 yrs fixed.

What to do?